The small business loan is over $750B annually, according to their 2020 reporting. These loans range from their signature government-backed 7(a) loans to microloans, and the funds can be used for business expenses from opening or expanding a business to equipment repairs to employee wages.

As a commercial lender, these loans can be an important way for your small business clients to grow their businesses and thrive. Here is everything you need to know about Small Business Administration (SBA) guaranteed loans, including who they are for, the borrowing terms and the impact the loan can have on a business.

Small Business Loan Overview

Small business loan falls under three categories: 7(a) loans, 504 loans and microloans. All have the potential to be life-changing for small business owners, and all are guaranteed in some form by the government.

The small business applies for an Small business loan through a bank or other community lending partner, and if approved, the SBA guarantees that they will pay the balance of the loan should the client default.

These similarities are the only ones, however. Each type of loan has different eligibility requirements, different uses and different repayment terms. Read on to learn the specifics.

7(a) Loans

7(a) loans are the most common loans funded by the Small business loan. These loans can be used to buy furniture, fixtures and supplies, restructure current business debt and for long- and short-term working capital. These loans are real-estate industry-friendly, and there are actually six different types of 7(a) loans that deal with domestic and international businesses.

7(a) loans are capped, and the lending limit is dictated by what specific loan you’re borrowing under. Lending caps are $350,000, $500,000 and $5M, though most loans come in under those caps. Eligibility factors include the business location, credit history and how the business earns its money. As a lender, your job is to help your client find the right 7(a) loan to fit their needs.

7(a) loans have both fixed and variable rate terms, with interest capped at the federal Prime rate, which is currently 6.25% as of October 6, 2022. Fixed-interest loans will have a consistent monthly payment while variable-rate loans can change at the lender’s discretion whenever the interest rate changes. The maximum lending terms for 7(a) loans are 25 years.

504 Loans

504 loans are long-term loans used to promote business and job creation and growth. A borrower can use a 504 loan to:

- Purchase existing buildings or land

- Purchase machinery

- Construct new buildings

- Improve, modernize or otherwise upgrade existing facilities

- Repair, improve, or update land, streets, parking and landscaping

A 504 loan cannot cover 7(a) territory, meaning that your clients cannot use a 504 loan to restructure or repay debt, to support the business through capital or inventory or to invest in real estate.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

504 loans require that the borrower put 10% down; the remainder is broken down with 40% funded through a community development company (CDC) and 50% funded through a third-party financial institution. 504 loans have 10 and 20-year terms, with interest on the CDC-held portion limited to around 3% of the total debt. The privately-held portion can be fixed or variable rate.

Businesses can borrow up to $5M, and have to meet the SBA requirements for classification as a small business. In addition, the business’s net worth can’t exceed $15M and they can only have a net income under $5M.

Microloans

Microloans are small loans of no more than $50,000 meant to help small businesses and certain kinds of not-for-profit childcare centers open and/or expand. Rather than fund the loans directly, the SBA provides money to community non-profits who administer the microloan program as well as provide mentorship and technical assistance to borrowers.

Borrowers can use microloans for capital, inventory, supplies, furniture, fixtures and more. They cannot use loan funds to purchase property or buildings or to pay existing debt.

Microloans have a maximum repayment term of six years, and interest rates and other terms vary depending on the community lender. As of this writing, interest on microloans ranges between 8-13%.

Pros and Cons of Small Business Loans

Small business loan offer qualified borrowers more competitive rates, lower fees, larger loan amounts and longer repayment terms than they would otherwise receive from private lenders. At the same time, your clients may find that the loans are difficult to both apply and qualify for. If they are eligible, SBA loans take between 30 and 90 days to fund, so if your client needs fast funding they will want to look elsewhere.

The other sticking point for a lot of businesses is the personal guarantee requirement. Depending on the loan, borrowers may have to put up a down payment, physical collateral or a personal guarantee from anyone with more than 20% ownership in the business.

Roundup

As a commercial lending professional, you owe it to your small business clients to at least be literate in the broad themes of Small business loan. Because these loans support all kinds of businesses, you’ll never know when the knowledge will help you or one of your clients.

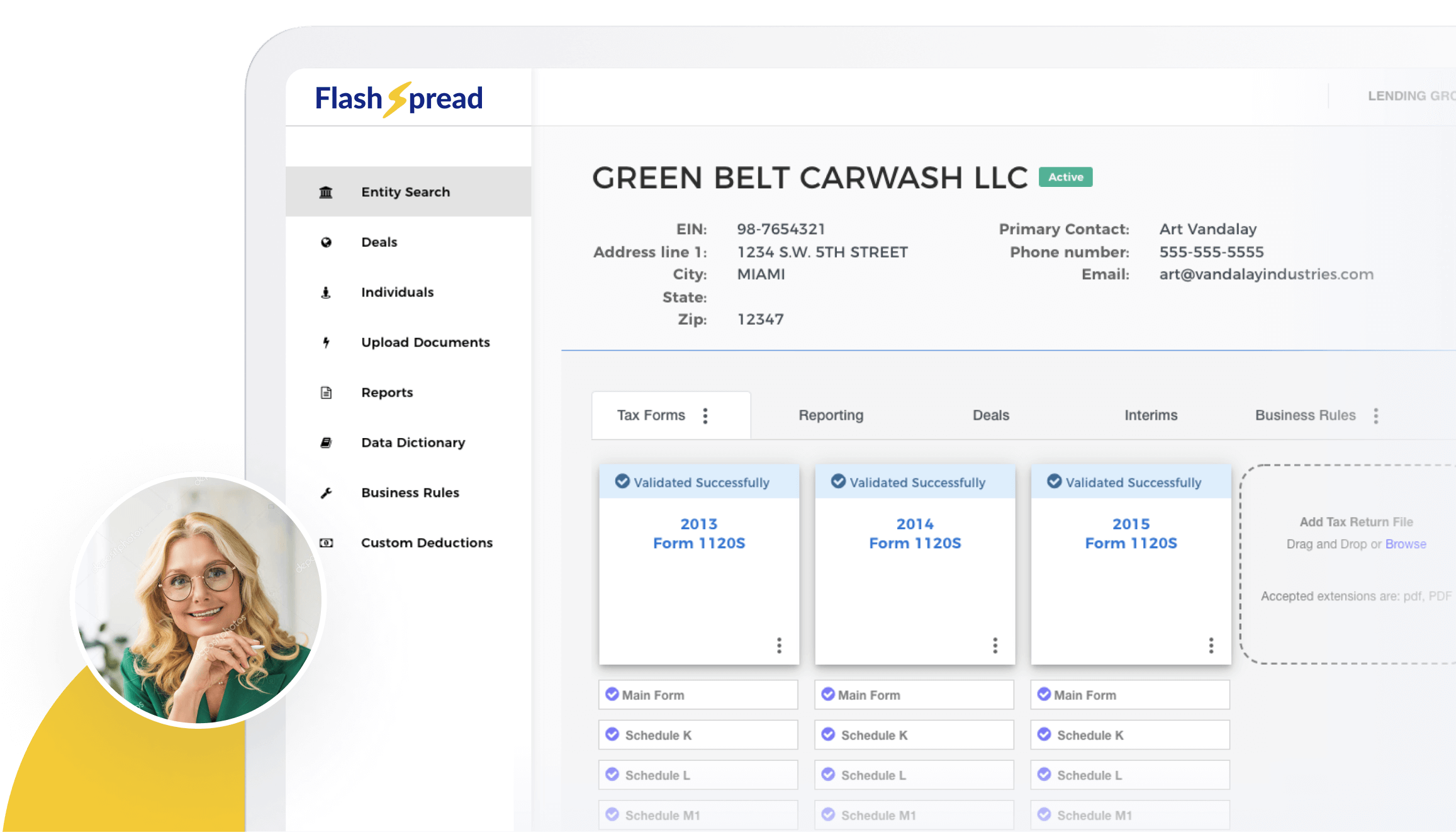

Financial institutions are using FlashSpread to qualify, underwrite and service Small business loan. Schedule a demo to learn more.