This release introduces the implementation of soft credit pull, offering borrowers the ability to check their credit scores without negative impacts on their credit history. Lenders can now perform soft-pull credit checks, providing a more cost-efficient alternative to hard credit pull. This update aims to empower borrowers with informed lending decisions while enabling lenders to optimize costs.

Implementation includes:

General Logic

- Available to all lenders.

- Support for all Credit Reporting Agencies (CRA).

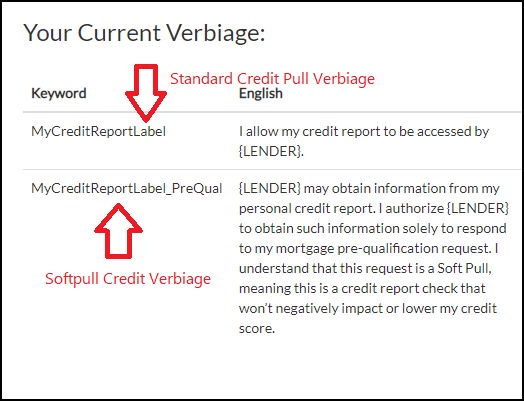

- During the application process, the consent for soft credit pull and hard credit pull is distinct.

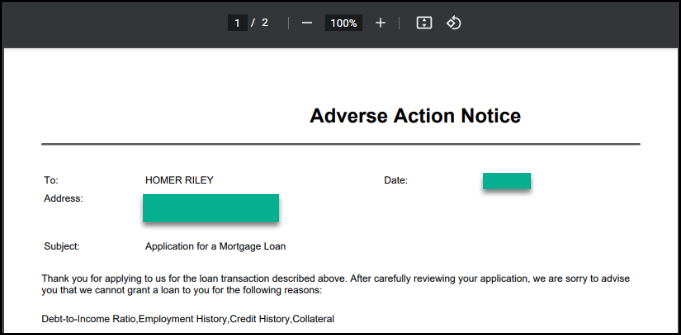

- If the lender performs a soft credit check and the loan is denied, the adverse action letter/email will not be generated. However, if a loan starts with a soft pull and later upgrades to a hard pull, adverse action will generate if there has been at least one hard pull on the loan.

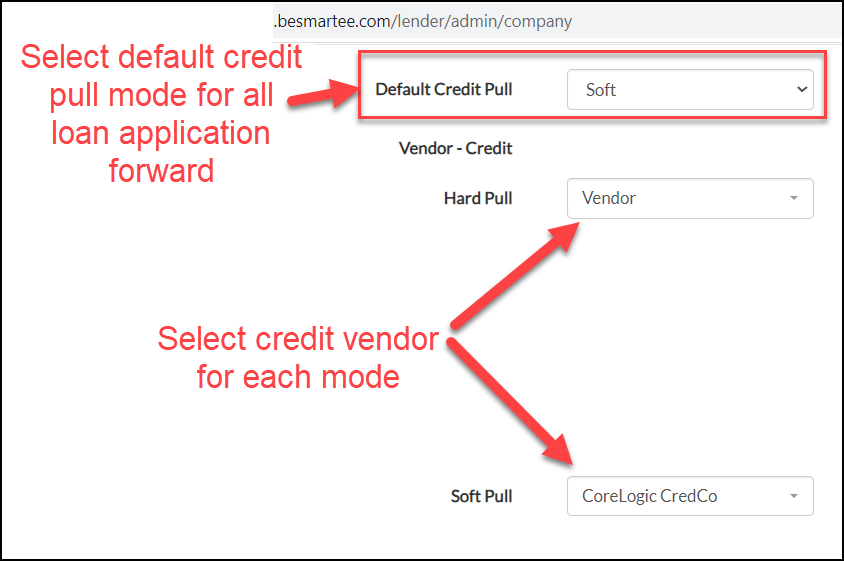

- The credit pull hierarchy cascades in the following order: Campaign → Loan Officer → Company.

User Interface Updates

- Soft-pull and hard-pull options can be set at the campaign, loan officer, or company level through the user interface (UI).

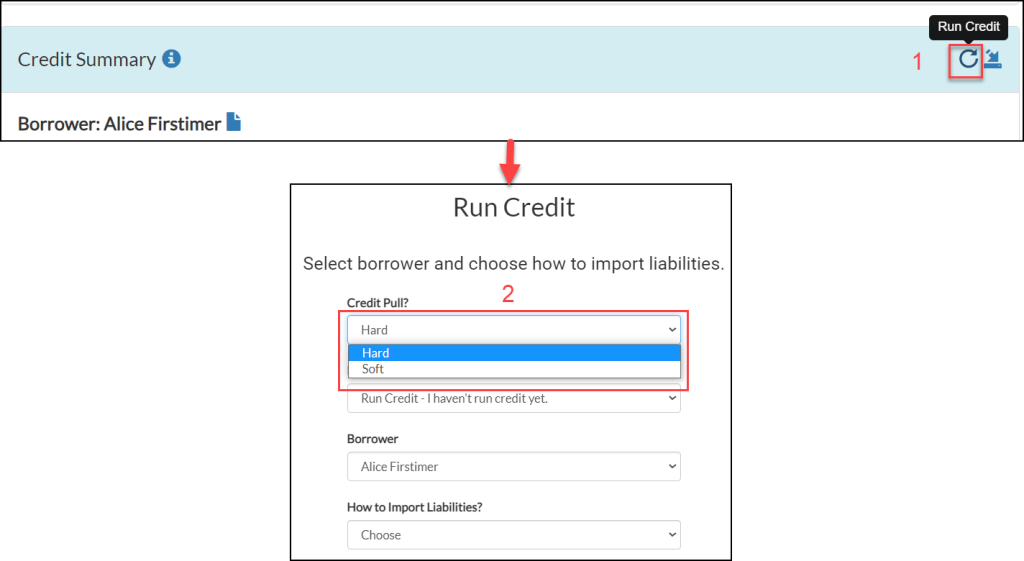

- The button Run Credit now presents a modal window when clicked, allowing the loan officer (LO) to choose between hard-pull and soft-pull options.

Reach out to your client success representative for more information on how to configure this new option.