Loan Origination Systems (LOS) excel at document intake, workflow tracking, and process visibility. Files are uploaded, statuses update, and applications move forward through the system as expected.

But turning those uploaded financials into decision-ready data is a separate step. Analysts still open PDFs, interpret tax forms, rekey numbers, and reconcile figures across spreadsheets before credit decisions can happen. This blog looks at what actually happens after documents enter the LOS, where spreading work truly lives, and how lenders can close that gap without slowing teams or adding headcount.

Key Insights at a Glance

- Most LOS platforms handle document routing, not financial spreading or analysis.

- The real work still happens manually in PDFs, spreadsheets, and local templates.

- This “hidden layer” slows decisions, introduces inconsistency, and increases risk.

- True automated spreading starts with data extraction and normalization, not just document storage.

- Tools like FlashSpread help close the gap by turning tax returns and financials into clean, standardized spreads in minutes.

Table of Contents

The Illusion of LOS Automation

From the outside, your LOS looks automated. Borrowers or relationship managers upload financials. The system timestamps the upload, updates the checklist, and moves the file to the next stage. Dashboards show the loan progressing in the pipeline.

On paper, the process looks digital and streamlined. But what the LOS isn’t doing is reading line items, interpreting tax forms, or calculating debt service coverage. It isn’t classifying Schedule C income, normalizing K-1s, or mapping 1120S data into a spread.

The LOS was built to intake, track, and route documents, not to extract, normalize, and analyze the numbers inside them. That gap between “file received” and “spread ready” is where manual work explodes.

What’s Actually Happening After Docs Are Uploaded

Here’s what the workflow looks like in many institutions once the documents land in the LOS:

- An analyst downloads tax returns or financials from the LOS to their desktop.

- They open a 1040, 1120, 1120S, or 1065 and start scrolling line by line.

- They flip between the PDF and a spreadsheet or in-house template.

- Every relevant line item is keyed in by hand or copy/pasted.

- Ratios and cash flow are calculated using formulas stored in local Excel files.

- Adjustments and add-backs vary depending on who built the template and how they prefer to spread.

- A narrative or memo is drafted from scratch, summarizing trends, risks, and strengths.

Only after all of that does a true credit decision start to take shape.

From the LOS view, it may look like the deal moved smoothly through “analysis.” But internally, analysts spent significant time doing work that many leaders assume is already automated.

Why This Hidden Manual Layer Matters

It might be tempting to say, “We’ve always done it this way.” But that hidden manual layer has real consequences for both risk and scale.

1. Time and throughput

When spreading takes an hour or more per file, analysts can only move so many deals through the pipeline, especially during busy seasons. As volume grows, turnaround times slow, and “backlog” becomes a constant theme.

2. Inconsistent results

If each analyst has their own template and approach to spreading, you end up with different interpretations of the same borrower. That makes side-by-side comparisons harder and introduces friction in credit committee discussions and audits.

3. Higher error risk

Anytime numbers are rekeyed manually, there’s a chance for mistakes. A single mis-typed digit can skew coverage ratios or cash flow, potentially changing the perceived risk of the deal.

4. Strain on teams

Analysts were hired to assess credit, not to act as human data pipes between PDFs and Excel. Too much manual prep contributes to burnout and makes it harder to retain and onboard talent.

In short, what looks like “automation” at the LOS level is often masking the most manual part of the process.

Signs Your LOS Isn’t Really Doing the Spreading

If you’re not sure how much of your spreading is still manual, a few questions can surface the reality quickly:

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

- Do analysts regularly export or download documents from the LOS to work in Excel?

- Are spreading templates stored on local drives, shared folders, or personal OneDrive accounts?

- Do credit managers spend review time checking inputs and formulas instead of focusing on risk position?

- Do two analysts sometimes arrive at slightly different spreads for the same borrower?

- Does spreading time come up as a bottleneck when you talk about cycle times or backlog?

If the answer is “yes” to several of these, your LOS is doing what it was built to do, route documents, but not what lenders increasingly need: automated, standardized, error-resistant spreading.

What True Automated Spreading Looks Like

True automated spreading doesn’t start with the LOS; it starts with the data inside the documents.

Instead of PDFs sitting in a queue until an analyst can get to them, an automation layer:

- Extracts data from tax returns and financials using OCR and machine learning.

- Organizes and maps that data into a consistent structure aligned to your spreading model.

- Calculates key metrics, including global debt service and other coverage measures.

- Normalizes outputs, so every borrower is evaluated using the same format and logic.

- Feeds standardized spreads back into your workflow and LOS environment.

In this model, analysts still review and adjust, but they start from a complete, structured spread, not a blank spreadsheet. The time shift is significant: less manual prep, more interpretation and judgment.

How FlashSpread Helps Close the Gap

This is exactly the gap FlashSpread was built to close.

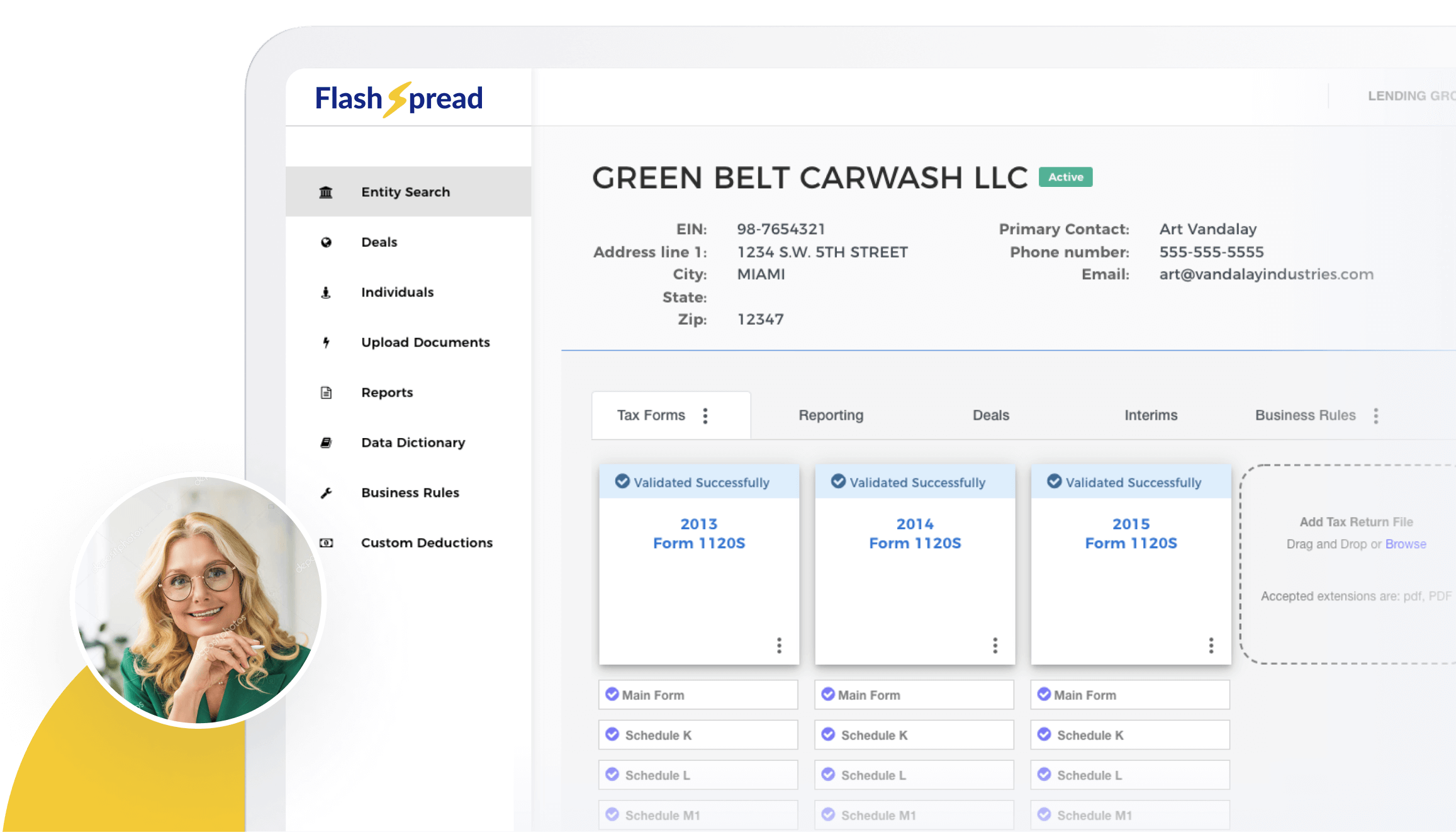

FlashSpread is an automated financial spreading solution for commercial and SBA lenders. It uses OCR and machine learning to extract complex data from tax returns and related schedules, then organizes that data into clean, standardized spreads in minutes instead of hours.

Based on the product info, FlashSpread:

- Automates extraction and spreading of financial data from forms like 1040, 1120, 1120S, 1065, and associated schedules.

- Handles both structured and unstructured documents, including scanned PDFs, with high accuracy.

- Calculates global debt service and supports monthly monitoring, giving teams a clearer view of repayment capacity.

- Reduces spreading time from roughly three hours to about five minutes, helping institutions scale volume without adding headcount.

- Integrates with leading LOS platforms so tax returns can flow directly from intake to automated spread and back into the credit workflow.

AI comes into play through machine learning models that improve classification and mapping over time, but the core value is simple: less manual data work, more time for actual credit analysis. FlashSpread doesn’t replace analysts; it gives them a stronger starting point and a cleaner, consistent view of borrower financials.

Q&A: Common Questions About LOS Platforms vs. Automated Spreading Solutions

Q. If my LOS already tracks documents and stages, do I really need separate automated spreading?

A. Yes. The LOS manages workflow and routing. Automated spreading handles the numbers inside the documents. They’re complementary, not redundant.

Q. Will automated spreading force us to abandon our current credit policies?

A. No. Good tools support your existing policies by standardizing how data is prepared and presented, without changing your underwriting criteria.

Q. Does automation remove analysts from the process?

A. Not at all. Automation reduces manual prep so analysts can spend more time on judgment-driven work, complex deals, and portfolio oversight.

Roundup

Most LOS platforms do exactly what they were designed to do: collect documents, track status, and move loans through defined stages. What they don’t do is the heavy lifting of financial spreading, extracting line items, normalizing tax returns, and calculating coverage metrics in a consistent way. That work is still happening in spreadsheets and templates, often hidden in the background and consuming far more analyst time than leaders realize.

By adding a true automated spreading layer, lenders can finally close the gap between “docs uploaded” and “data ready.” Instead of manually bridging that space, analysts start with clean, standardized financials and focus on what they do best: assessing risk, supporting borrowers, and strengthening portfolio performance in every market cycle.

Curious how automation can close the gap between your LOS and real spreading workflows? Explore how FlashSpread can help turn manual prep time into faster, more confident credit decisions.