In commercial lending, credit risk is unavoidable. But in today’s environment, marked by rising interest rates, inflationary pressures, and an uneven recovery across industries, those risks have grown more complex. For commercial lenders, the challenge is no longer just evaluating an individual borrower’s creditworthiness. It’s about protecting the health of an entire portfolio while still keeping up with borrower demand for speed, transparency, and flexibility.

When risk isn’t managed effectively, the consequences multiply: delayed decisions, higher default rates, and missed opportunities to grow. Moreover, regulatory scrutiny is increasing, and lenders are expected to document risk practices thoroughly while remaining competitive.

So how can lenders navigate uncertainty while maintaining strong portfolio health? The answer lies in combining smarter credit risk practices with operational efficiency that helps lenders and borrowers alike.

Key Insights at a Glance

- Gain clearer visibility into borrower and portfolio risk

- Standardize credit evaluations for consistency

- Cut errors and speed up decisions with smarter workflows

- Monitor portfolios continuously to detect early warning signs

- Balance speed with diligence to maintain borrower trust

Table of Contents

The Shifting Risk Landscape

Market uncertainty has reshaped how lenders view credit risk. Borrowers are contending with higher operating costs, shifting consumer demand, and in some industries, declining revenues. Even strong businesses can appear riskier on paper.

For commercial lenders, this creates three big challenges:

- Higher exposure risk: Concentrations in certain industries or geographies can become liabilities when economic conditions change. For instance, a lender with heavy exposure to hospitality or retail may see sudden spikes in defaults if economic conditions deteriorate.

- Borrower strain: Rising interest costs eat into cash flow, making repayment harder for borrowers that previously had healthy margins.

- Competitive pressure: While risk is up, borrower expectations for speed haven’t changed, lenders that take too long risk losing good deals to faster competitors.

In this environment, portfolio health depends on how quickly lenders can identify risks, adapt underwriting strategies, and make decisions with confidence.

Why Portfolio Health Starts With Smarter Credit Risk Management

A healthy loan portfolio isn’t built on luck, it’s built on disciplined, consistent credit risk management. That starts with a deeper look at borrowers and a broader view of portfolio exposure.

Key practices include:

- Holistic borrower analysis: Go beyond financial ratios. Include industry outlooks, borrower track records, and sensitivity to market shifts.

- Continuous monitoring: Risk doesn’t end at origination. Monitoring borrower performance and stress-testing portfolios helps catch red flags before they become losses. Tools like rolling financial ratio dashboards or scenario analyses can reveal emerging stress points and allow preemptive action.

- Balancing speed with diligence: The pressure to respond quickly is real, but skipping steps in spreading or analysis creates blind spots that weaken portfolio health.

By embedding these practices, commercial lenders build resilience into their portfolios while protecting both their balance sheet and borrower relationships. This approach also enables lenders to communicate more confidently with stakeholders about risk exposure, supporting strategic growth and investor confidence.

Turning Efficiency Into a Risk Advantage

One of the biggest hidden risks in commercial lending is inefficiency. Manual spreading of financial statements is slow, error-prone, and inconsistent across staff. A single missed detail or calculation can distort the risk profile of a deal and, over time, harm the overall portfolio.

More importantly, inefficiency drains resources:

- Time: Credit analysts can spend hours re-entering data instead of evaluating deals.

- Accuracy: Manual processes increase the risk of mistakes that skew decisions.

- Opportunity cost: Slow turnaround times frustrate borrowers and can cost lenders good deals.

Improving efficiency is not just about doing things faster but about strengthening portfolio health. When spreading and analysis are accurate and timely, lenders can:

- Identify high-risk borrowers earlier

- Maintain consistent standards across the portfolio

- Free underwriters to focus on complex, judgment-driven decisions

Efficiency, in other words, becomes a risk advantage. It allows lenders to manage higher volumes without compromising quality, helping maintain profitability even during volatile market periods.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Q&A: Common Credit Risk Challenges

Q: How can lenders spot early warning signs of borrower stress?

A: Continuous monitoring of cash flow, debt service ratios, and revenue trends is key. Early detection lets lenders intervene proactively, offering support or restructuring before a loan becomes delinquent.

Q: What role does portfolio diversification play?

A: Diversifying across industries, geographies, and loan sizes reduces exposure to sector-specific downturns. Even when individual borrowers struggle, a diversified portfolio mitigates overall risk.

Q: How do rising interest rates impact credit risk?

A: Higher rates can squeeze borrowers’ margins, increasing default probability. Lenders need to reassess debt service coverage and consider stress tests under multiple rate scenarios.

Q: Is speed really a risk factor?

A: Yes. Slow processes can lead to missed opportunities and borrower attrition. Conversely, rushing decisions without thorough analysis can increase default risk. The key is balancing efficiency with diligence.

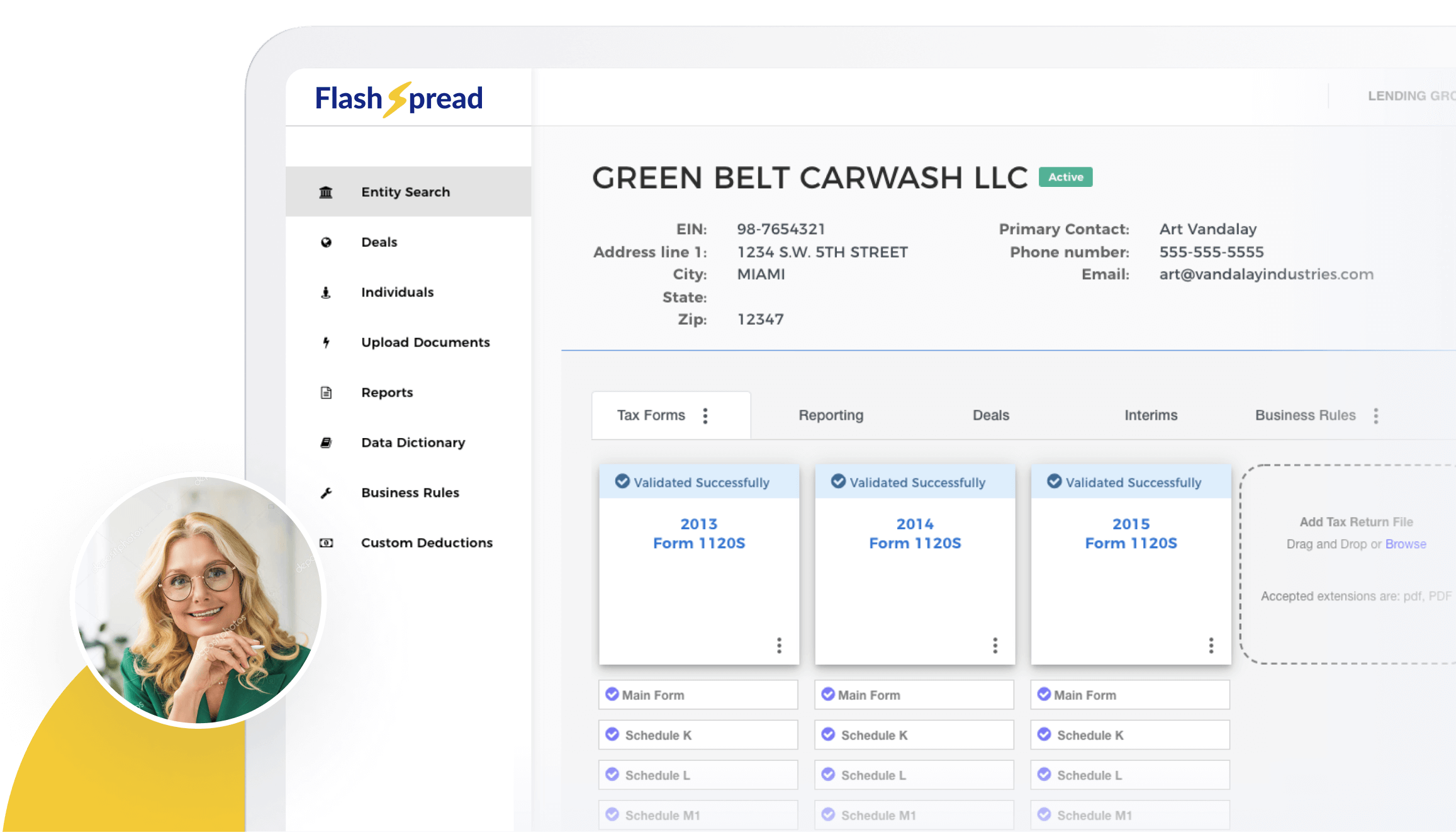

Efficient Spreading, Stronger Decisions

Manual spreading has long been one of the bottlenecks in commercial lending. Hours are spent rekeying tax returns, reconciling inconsistencies, and recalculating coverage ratios—time that slows portfolio reviews and creates room for costly errors.

FlashSpread helps lenders move past those manual steps by extracting and organizing data from tax returns and scanned financials in minutes. Instead of underwriters chasing numbers, they can focus on what matters most: identifying risk patterns and making confident credit calls.

With FlashSpread, lenders can:

- Eliminate repetitive data entry that delays reviews

- Access debt service coverage and other key ratios faster

- Maintain more consistent evaluations across borrowers and deals

- Free staff to spend more time on complex, judgment-driven decisions

- Standardize reports and spreadsheets, making audits and regulatory reviews easier

The result? Faster, more accurate spreading that supports healthier portfolios and reduces the risk of overlooked red flags.

Roundup

Credit risk is part of every commercial lender’s reality but in volatile markets, the stakes are higher. Portfolio health now depends on how well lenders can combine deeper borrower insights with operational efficiency that reduces errors and accelerates decision-making.

By focusing on visibility, consistency, and efficiency, lenders can protect themselves against uncertainty while still meeting the borrower’s demand for speed and service. And with automation tools like FlashSpread, they can strengthen credit risk management without adding complexity to their workflows.

Ready to reduce errors and make quicker, data-driven lending decisions? Explore FlashSpread and reach out to our team today.