In commercial lending, portfolio risk is often discussed in terms of exposure limits, concentration thresholds, and performance metrics. But long before those indicators appear in reports, portfolio risk begins much earlier—at the moment business financials enter the credit process.

Income statements and balance sheets form the basis of credit decisions, monitoring, and reporting. When these documents are reviewed inconsistently or structured poorly at intake, the effects don’t stop at underwriting. They surface later in portfolio monitoring, risk trending, and decision confidence. Over time, small inconsistencies compound into larger blind spots.

This blog explores how early handling of business financials shapes portfolio risk downstream, why structure matters beyond origination, and what lenders can do to strengthen portfolio health without adding friction to the credit process.

Key Insights at a Glance

- Portfolio risk often originates before underwriting begins

- Inconsistent business financial structure distorts downstream analysis

- Early categorization impacts monitoring and trend accuracy

- Small intake issues compound across portfolios over time

- Strong structure improves both decision confidence and long-term oversight

Portfolio Risk Starts Earlier Than Most Lenders Realize

Portfolio risk is typically evaluated after loans are booked. Metrics such as delinquency rates, exposure by industry, and cash flow trends help lenders understand how risk is evolving. But these metrics depend entirely on the quality and consistency of the underlying financial data.

If business financials are structured differently across borrowers or periods, portfolio-level analysis becomes unreliable. Two borrowers with similar financial profiles may appear very different simply because their income statements were categorized differently or their reporting periods were handled inconsistently. In this way, portfolio risk isn’t just about borrower behavior; it’s also about data integrity.

What often goes unnoticed is how early-stage inconsistencies limit a lender’s ability to take action later. When portfolio reporting relies on unevenly structured business financials, risk teams are forced to rely on partial signals or manual adjustments to interpret trends. This not only slows response times but also increases the likelihood that emerging issues go undetected until they become material.

Over time, this weakens confidence in portfolio analytics. Instead of serving as a proactive risk management tool, reporting becomes reactive, used to explain outcomes rather than prevent them. Strong early structure helps ensure that portfolio insights are timely, comparable, and actionable, especially as loan volumes grow and credit conditions shift.

How Early Structure Influences Long-Term Monitoring

Once a loan is approved, business financials don’t disappear. They continue to feed:

- Ongoing monitoring

- Covenant tracking

- Trend analysis

- Portfolio reporting

If line items were miscategorized or left uncategorized during initial review, those gaps follow the loan forward. Missing or inconsistent data can distort debt service coverage trends, mask deteriorating performance, or create false signals of improvement.

Early structure ensures that financial data behaves predictably across time. When periods are aligned and categories are consistent, lenders can compare performance more confidently, identify meaningful changes, and respond to risk earlier rather than later.

The Compounding Effect of Small Inconsistencies

A single misclassification might seem minor at the deal level. But across dozens or hundreds of loans, these inconsistencies multiply.

Common examples include:

- Operating expenses are categorized differently across borrowers

- Revenue is grouped inconsistently year over year

- Periods included for some borrowers but excluded for others

At scale, this makes portfolio comparisons unreliable. Credit teams spend more time explaining discrepancies than evaluating risk, and leadership loses confidence in reporting outputs.

What begins as a small intake issue becomes a systemic portfolio challenge, especially as portfolios grow and diversify.

Why Underwriting Can’t Fix Structural Issues Later

Underwriters are tasked with evaluating risk, not rebuilding financial structure. When poorly structured business financials reach underwriting, teams face a difficult tradeoff: pause the deal to fix upstream issues or move forward with imperfect data.

Either choice carries risk. Fixing issues late slows decisions and frustrates borrowers. Ignoring them weakens the foundation of the credit decision and introduces uncertainty into future monitoring.

This is why early structure matters. Addressing inconsistencies at intake reduces pressure downstream and allows underwriting to focus on judgment rather than cleanup.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Standardization as a Risk Management Tool

Standardization is often discussed as an efficiency play, but it’s also a risk control mechanism. When business financials follow consistent categorization and reporting structures:

- Ratios are comparable across borrowers

- Trends are easier to interpret

- Monitoring thresholds become more meaningful

Standardization doesn’t eliminate judgment. It ensures that judgment is applied to data that behaves consistently across the portfolio.

From a portfolio perspective, standardization also enables scale. As lenders expand into new markets, industries, or borrower segments, a consistent financial structure allows risk teams to evaluate performance without reinventing analysis frameworks. This makes it easier to spot concentration risk, compare borrower cohorts, and apply consistent monitoring thresholds across the portfolio.

Without this foundation, growth introduces complexity faster than teams can manage it. Standardized business financials act as a stabilizing layer, supporting both day-to-day credit decisions and long-term portfolio strategy.

Q&A: Portfolio Risk and Business Financial Structure

Q: Isn’t portfolio risk driven mostly by economic conditions?

A: Economic conditions matter, but data quality determines how clearly those risks are seen. Poor structure can hide or exaggerate risk signals.

Q: Can monitoring tools compensate for weak intake structure?

A: Monitoring tools rely on the same underlying data. If intake data is inconsistent, monitoring outputs will be too.

Q: Does this really affect long-term portfolio health?

A: Yes. Consistent structure improves comparability, trend analysis, and early warning signals, all of which support stronger portfolio management.

Supporting Better Structure Earlier in the Process

Improving portfolio risk outcomes starts by strengthening how business financials are handled before underwriting. Manual processes make this difficult at scale, especially when documents vary widely in format and structure.

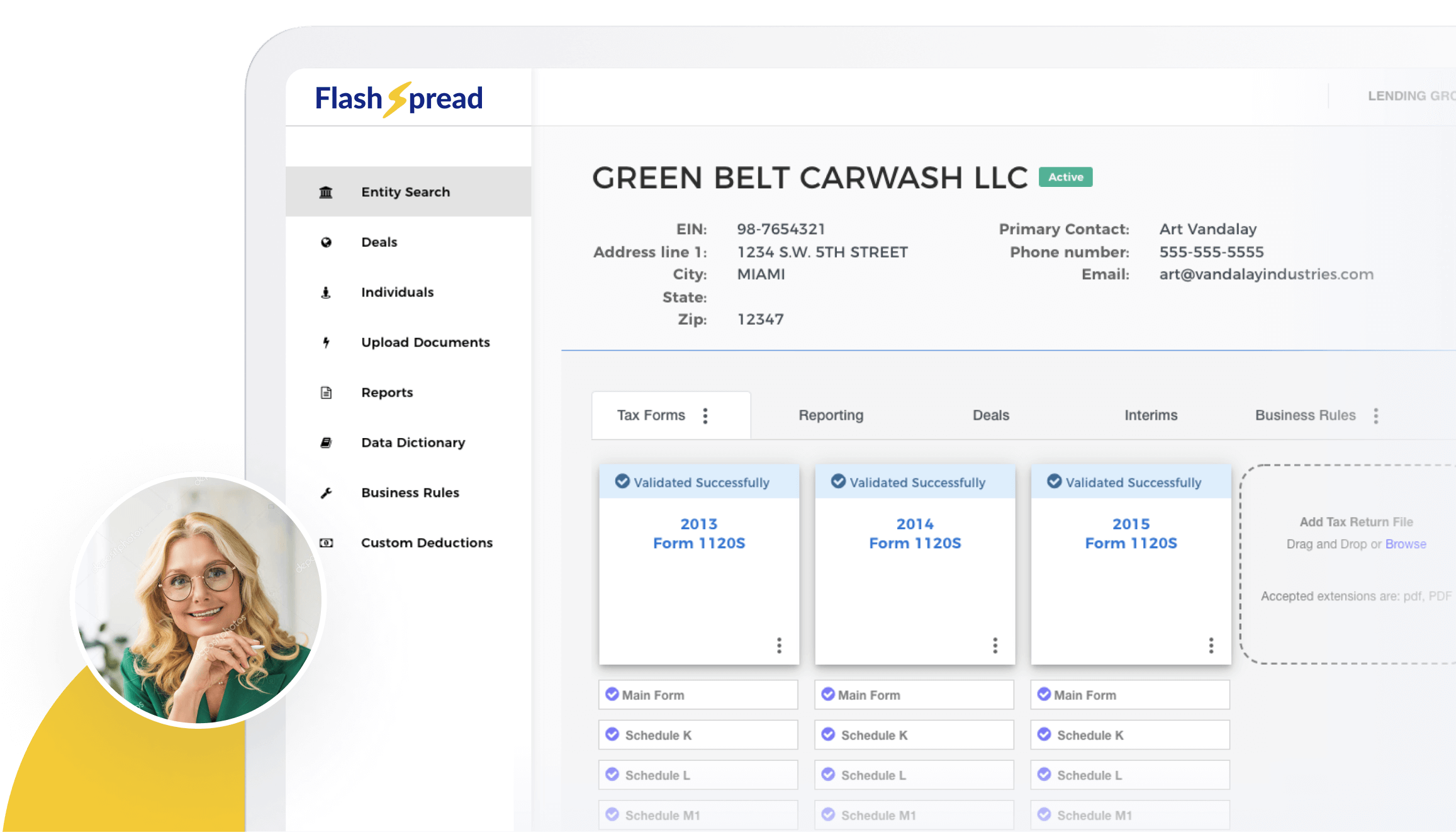

Tools like FlashSpread support this early-stage work by applying advanced OCR and machine learning to extract and organize data from income statements and balance sheets. Instead of relying solely on manual re-keying, financial data enters the workflow in a more consistent, structured format.

As teams review and categorize line items, FlashSpread’s machine learning capabilities begin to recognize common patterns and categorization behavior, helping streamline future reviews. This supports:

- More consistent financial structure across borrowers

- Earlier identification of missing or misaligned data

- Cleaner inputs for downstream monitoring and reporting

The goal isn’t to replace credit judgment. It’s to ensure that judgment is based on reliable, consistently structured financial data that supports portfolio-level insight.

Taken together, these dynamics highlight an important shift in how lenders should think about portfolio risk. It’s no longer enough to focus solely on downstream controls and monitoring tools. The quality of portfolio insights depends on the quality of financial structure established much earlier in the credit lifecycle.

Roundup

Portfolio risk doesn’t begin at monitoring; it begins at intake. How business financials are structured early in the credit process shapes everything that follows, from underwriting confidence to long-term portfolio oversight.

When structure is inconsistent, risk signals blur. When structure is sound, trends emerge more clearly, decisions move faster, and portfolios become easier to manage at scale.

By strengthening early review practices and supporting them with better structure, lenders can reduce downstream risk without slowing the credit process.

If portfolio reporting and monitoring feel harder than they should, it may be time to look upstream. Learn how FlashSpread helps lending teams bring structure to business financials earlier—so portfolio risk is easier to see later.