In commercial lending, few terms are used more loosely than credit-ready. Business financials are uploaded, attached to a deal, and passed along with the assumption that underwriting can begin. But for credit desks and underwriting teams, “uploaded” and “credit-ready” are not the same thing.

Income statements and balance sheets arrive in many forms: different accounting systems, inconsistent line item structures, varying reporting periods, and varying levels of completeness. Before any credit decision can be made, these documents must be reviewed, validated, organized, and normalized. That work happens largely inside the credit desk, often quietly, and often under pressure.

This blog explores what credit-ready business financials actually mean from a credit desk perspective, why so many delays originate before underwriting begins, and how lenders can improve decision quality by strengthening this early stage of the credit process.

Key Insights at a Glance

- Credit-ready business financials require validation, categorization and consistency, not just document upload

- Most review delays occur before underwriting, during intake and preparation

- Inconsistent formats and reporting periods slow credit desk decisions

- Clear standards reduce rework and improve confidence in financial analysis

- Earlier structure leads to faster, more consistent credit decisions

Table of Contents

Why “Credit-Ready” Means Different Things to Different Teams

For relationship managers or loan officers, credit-ready may simply mean that financials have been received from the borrower. For underwriting, it often means numbers are visible and ratios can be calculated. For the credit desk, however, credit-ready means something more specific: the data is accurate, structured, comparable, and ready to support a decision without additional clarification.

This disconnect creates friction. Files move forward too early, only to stall when inconsistencies are discovered. Credit desks are forced to send deals back for clarification, adjust numbers mid-review, or reconcile discrepancies under tight timelines. These loops slow approvals and frustrate both internal teams and borrowers.

Defining credit-ready business financials more clearly helps align expectations across the lending workflow and reduces unnecessary back-and-forth.

What Credit Desks Actually Do Before Underwriting Begins

Before a credit analyst evaluates risk, business financials typically go through several critical steps. These steps are often underestimated or invisible to teams upstream, yet they are essential for decision integrity.

1. Validation

Credit desks must confirm that totals tie correctly, subtotals roll up as expected, and values reflect what appears on the original document. Parent-child relationships in financial statements matter, and when they don’t align, analysts must investigate.

2. Reorganization

Business financials are rarely presented in a standardized way. Line items may be grouped differently, labeled inconsistently, or buried under non-standard headings. Reorganizing these line items ensures financials align with internal reporting and analysis frameworks.

3. Categorization

For financials to flow into downstream reports, ratios, and monitoring tools, line items must be categorized correctly. Uncategorized or miscategorized items can distort analysis or disappear entirely from reporting.

Until these steps are completed, financials may be visible, but they are not credit-ready.

The Role of Reporting Periods in Credit Readiness

Unlike tax returns, business financials can include multiple reporting periods: monthly, quarterly, or annual. Some documents include overlapping periods or partial year data. Others mix trailing twelve-month figures with year-end totals.

Credit desks must decide which periods to include in analysis and which to exclude. This decision directly impacts ratio calculations, trend analysis, and risk assessment. Using the wrong period can lead to misleading conclusions about cash flow stability or growth.

Credit-ready financials clearly define which periods are in scope, which are excluded, and why. Without this clarity, underwriting decisions rest on unstable ground.

Why Credit Readiness Breaks Down at Scale

As loan volume increases, weaknesses in business financial review processes become more visible. What works for a handful of deals quickly breaks down under pressure.

Common challenges include:

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

- Analysts applying different interpretations to similar line items

- Inconsistent categorization across borrowers or periods

- Manual review steps that don’t scale with volume

- Increased reliance on tribal knowledge instead of documented standards

Without standardized workflows, credit desks spend more time reconciling data than evaluating risk. This not only slows decisions but also increases variability across the portfolio.

The Cost of Sending Non–Credit-Ready Financials to Underwriting

When business financials reach underwriting before they are truly credit-ready, the cost shows up in multiple ways:

- Rework: Analysts must pause risk evaluation to fix upstream issues

- Delays: Deals stall while data is corrected or clarified

- Confidence gaps: Committees question the reliability of the numbers

- Borrower friction: Additional document requests erode trust

Over time, these inefficiencies reduce throughput and strain relationships. Strengthening credit readiness earlier helps preserve momentum throughout the lending process.

Q&A: Common Credit Desk Questions About Credit Readiness

Q: Aren’t these review steps part of underwriting anyway?

A: While underwriting evaluates risk, credit readiness ensures the data being evaluated is accurate and structured. Without this foundation, underwriting decisions become less reliable.

Q: Can experienced analysts compensate for poor structure?

A: Experience helps, but it doesn’t eliminate the risk of inconsistent interpretation or manual error, especially at scale.

Q: What happens if some data remains uncategorized?

A: Uncategorized items often don’t flow into downstream reports, which can distort ratios and trend analysis without being immediately obvious.

Supporting Credit-Ready Business Financials With Better Structure

Credit desks need tools and processes that support accuracy and consistency without slowing teams down. Manual review alone makes it difficult to maintain standards across large volumes of deals.

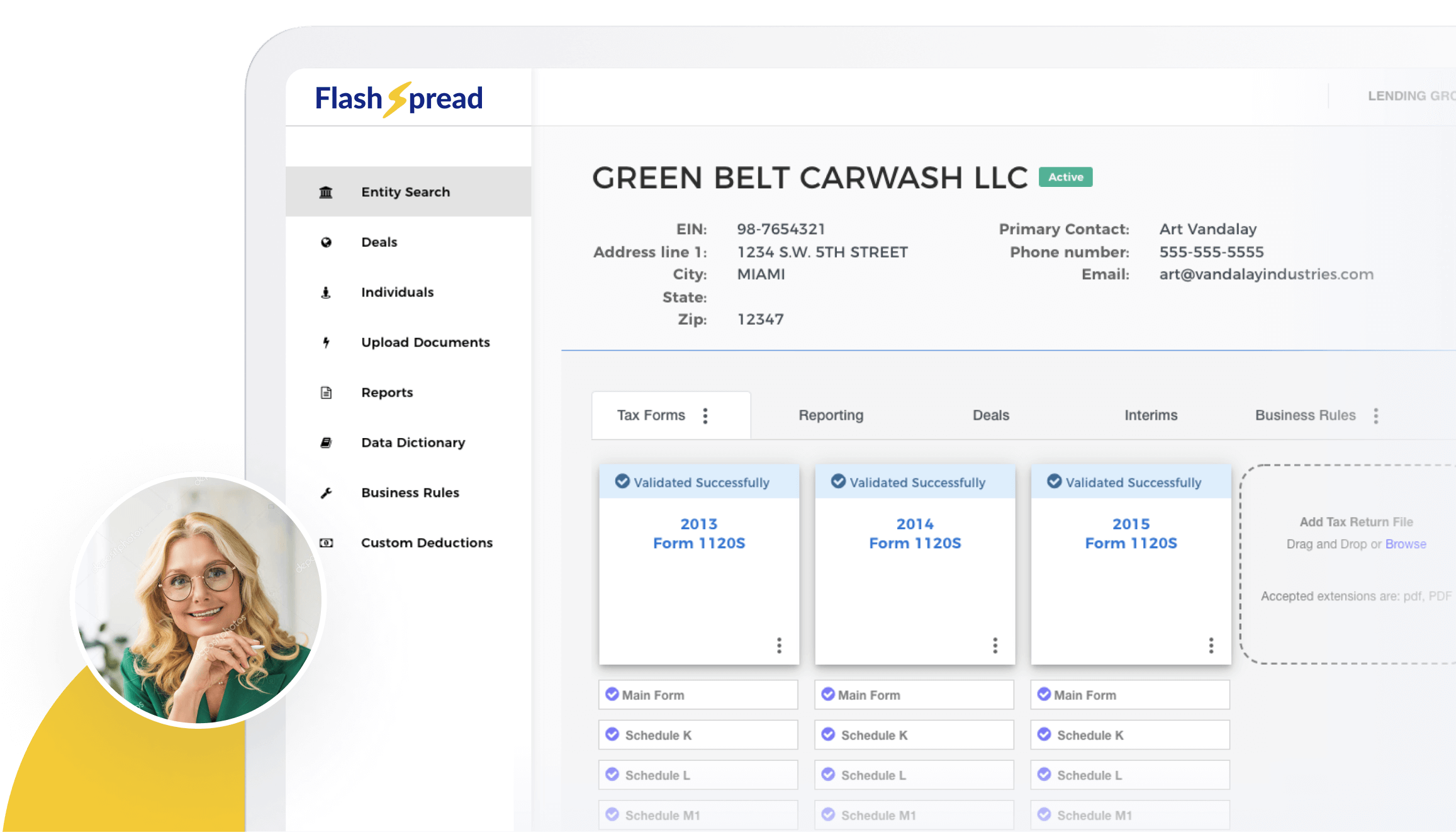

This is where structured workflows can help. Platforms like FlashSpread support credit desks by organizing business financial data earlier in the process. Using advanced OCR and machine learning, financial data from income statements and balance sheets is extracted and normalized into a consistent structure.

For credit teams, this means:

- Less time spent rekeying and reorganizing data

- More consistent categorization across borrowers and periods

- Clearer visibility into which data is ready for analysis

- Faster progression from intake to underwriting

The goal isn’t to remove judgment from the process. It’s to ensure judgment is applied to reliable, credit-ready information.

Roundup

Credit-ready business financials are not defined by upload status or document presence. They are defined by accuracy, structure, and consistency. For credit desks, this distinction matters.

When business financials are reviewed, validated, and categorized before underwriting begins, decisions move faster and with greater confidence. Rework declines, portfolio oversight improves, and borrower experience benefits from fewer delays.

As lending environments grow more complex and volumes increase, strengthening credit readiness isn’t optional. It’s a prerequisite for scalable, high-quality credit decisioning.

If your credit desk is spending too much time preparing data instead of evaluating risk, it may be time to rethink how business financials become credit-ready. Learn how FlashSpread helps teams move from documents to decisions with greater consistency and confidence.