For commercial lenders, business financials are essential to every credit decision. Income statements and balance sheets drive cash flow analysis, risk ratings, pricing, and approval outcomes.

Yet despite their importance, these documents often arrive in the least helpful format possible: PDFs. At first glance, reviewing business financials might seem straightforward. Upload the documents, scan for key numbers, and move on to underwriting.

In reality, turning borrower-provided PDFs into credit-ready data is one of the most time-consuming and error-prone parts of the lending process.

This is because business financials are rarely standardized. Formats vary by accounting system, industry, preparer, and reporting period. Line items shift from one statement to the next. Multiple periods appear in a single document. And critical context is often buried in subtotals or footnotes.

This blog breaks down what actually happens between PDF upload and credit decision. We’ll walk through the hidden work required to review business financials accurately, why this step slows down credit desks, and how lenders can streamline the process without sacrificing rigor or control.

Key Insights at a Glance

- Reviewing business financials is more than reading numbers; it requires validation, structure, and context

- PDFs introduce variability that slows analysis and increases error risk

- Most delays happen before underwriting, during document review and preparation

- Clean, standardized financial data is critical for accurate credit decisions

- Improving this early stage can significantly reduce downstream rework and delays

Why Business Financials Are So Hard to Review

Unlike tax returns, business financial statements are not standardized. Two borrowers with identical financial performance can submit income statements that look completely different.

Some of the most common challenges lenders face include:

- Inconsistent layouts: Line items may be grouped differently or labeled inconsistently across documents

- Varying reporting periods: Monthly, quarterly, and annual statements may all appear in the same file

- Multiple entities: Borrowers often submit separate statements for related businesses

- Missing context: Subtotals, adjustments, and parent-child relationships are not always clear

As a result, credit teams spend significant time interpreting the structure of a document before they can even begin evaluating the numbers. This interpretation work is rarely visible in pipeline metrics, but it’s one of the biggest drivers of slow turnaround times.

Step 1: Uploading Is the Easy Part

Uploading business financials into a system is rarely the bottleneck. Most lenders can accept PDFs through a portal, email, or document upload screen without issue.

The real work begins after upload.

Once a document is in the system, lenders must determine:

- Which entity the document belongs to

- What reporting period(s) it covers

- Whether the document is complete and usable

- How it should flow into downstream analysis

Without accurate entity association and period identification, even perfectly extracted data can create confusion later in the credit process.

Step 2: Extracting Data From PDFs

PDFs are designed for presentation, not analysis. Extracting usable financial data from them requires translating static content into structured values.

When this process is manual, analysts must:

- Locate each relevant line item

- Identify whether values are positive or negative

- Confirm totals and subtotals

- Re-key numbers into spreadsheets or systems

This step is highly repetitive and vulnerable to transcription errors, especially when documents are lengthy or poorly formatted. Even small mistakes at this stage can distort ratios, cash flow analysis, and risk assessments.

Step 3: Validating the Numbers

Extraction alone is not enough. Once values are captured, they must be validated to ensure accuracy.

For business financials, validation typically involves:

- Confirming that child line items roll up correctly to parent totals

- Verifying that assets equal liabilities plus equity

- Checking that revenue and expense subtotals align with reported totals

When discrepancies appear, analysts must pause their work, trace the source of the issue, and reconcile differences manually. This back-and-forth is a major contributor to rework and delays.

Step 4: Reorganizing and Structuring Line Items

Because business financials are not standardized, lenders often need to reorganize line items to make statements comparable across borrowers and time periods.

This can include:

- Adjusting parent-child relationships between line items

- Removing irrelevant or duplicate entries

- Adding missing line items required for internal analysis

- Reordering sections to align with reporting standards

Without this normalization step, downstream reporting and comparisons become unreliable. However, doing this manually across dozens or hundreds of deals quickly becomes unsustainable.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Step 5: Categorizing for Credit Analysis

Categorization is one of the most critical and overlooked steps in reviewing business financials.

Each line item must be mapped to a category that supports:

- Ratio calculations

- Cash flow analysis

- Portfolio reporting

- API exports and integrations

If line items remain uncategorized or inconsistently categorized, they may be excluded from reports or misrepresented in analysis. This directly impacts credit decisions and portfolio oversight.

Why This Process Slows Credit Desks Down

Individually, each step may seem manageable. Together, they create a compounding bottleneck.

Credit desks often find themselves:

- Reviewing the same document multiple times

- Fixing errors introduced earlier in the process

- Waiting on clarification from borrowers or analysts

- Repeating work across similar deals

The result is longer cycle times, frustrated teams, and delayed decisions that impact both revenue and borrower experience.

Q&A: What Credit Teams Commonly Ask

Q: Why does reviewing business financials take longer than tax returns?

A. Because business financials lack a standardized structure. Each document requires interpretation, validation, and categorization before it can be analyzed.

Q: Can experienced analysts eliminate these delays?

A. Experience helps, but it doesn’t remove variability. Manual processes introduce risk regardless of skill level, especially at scale.

Q: Where should lenders focus to speed things up?

A. Early-stage document review and preparation. Improving accuracy and structure at the front of the workflow reduces downstream rework significantly.

Making Business Financials Credit-Ready Faster

The key to faster credit decisions isn’t rushing underwriting. It’s ensuring that financial data enters the credit workflow clean, validated, and structured.

This means:

- Reducing manual re-keying

- Validating totals and relationships early

- Normalizing data for consistency

- Applying repeatable categorization standards

When these steps are handled efficiently, underwriters can focus on judgment and risk assessment instead of data cleanup.

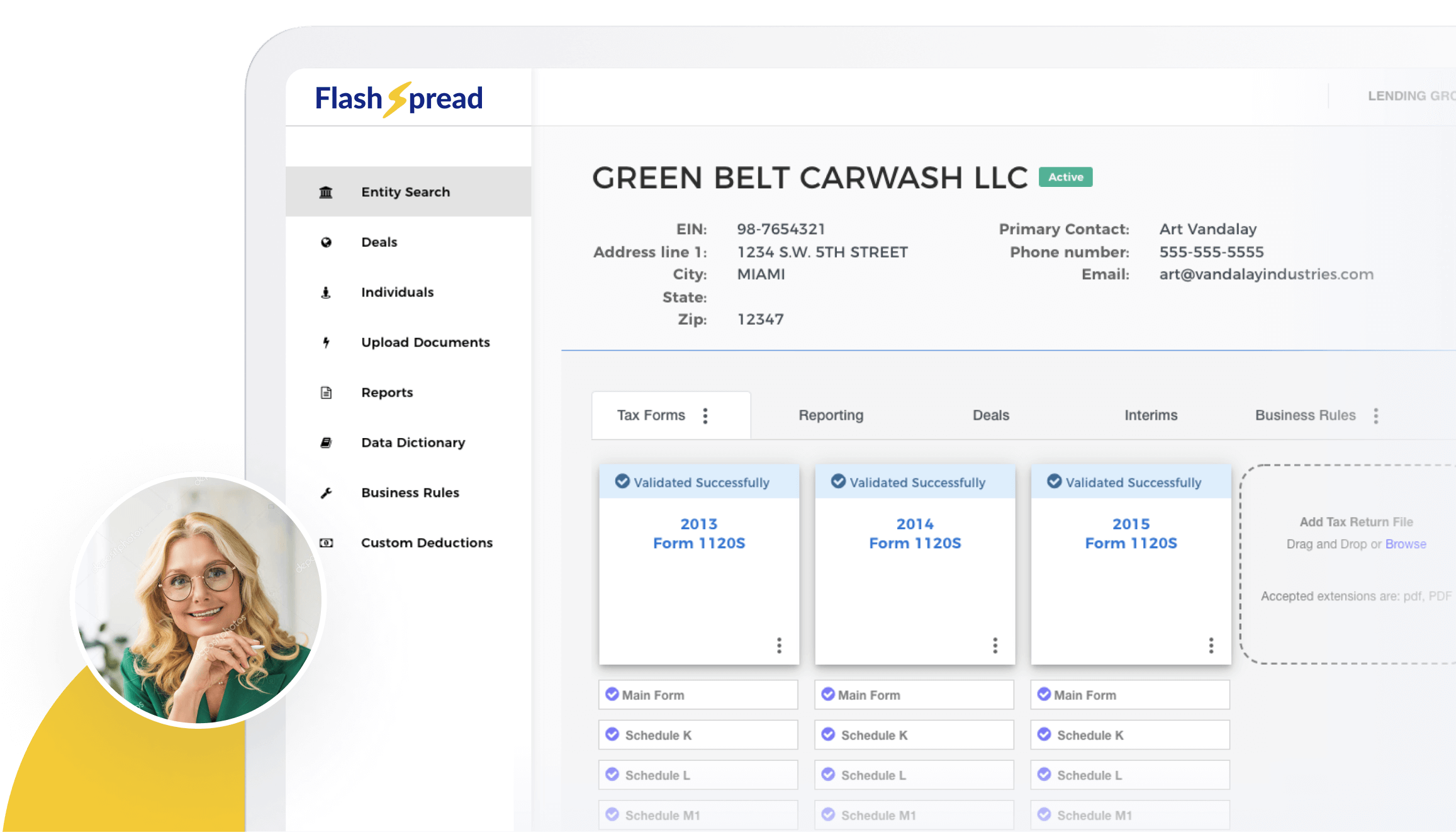

Where FlashSpread Fits Into the Workflow

FlashSpread supports this process by helping lenders move business financials from PDF to credit-ready data more efficiently.

Using advanced OCR and machine learning, FlashSpread extracts and organizes financial data from structured, unstructured, and scanned documents, including income statements and balance sheets. Its AI-driven approach learns common document patterns and categorization behavior over time, helping standardize how data enters the credit workflow.

In practice, this allows lenders to:

- Reduce manual data extraction from PDFs

- Validate totals and relationships earlier in the process

- Normalize line items for consistent reporting

- Spend less time reworking spreads and more time evaluating risk

The goal isn’t to replace analyst expertise, but to remove the repetitive, error-prone work that slows credit desks down.

Roundup

Reviewing business financials is one of the most critical steps in commercial lending, yet it’s also one of the most complex. From extraction and validation to structuring and categorization, turning PDFs into credit-ready data requires far more effort than most borrowers realize.

Lenders that improve this early stage gain more than speed. They reduce errors, improve consistency, and create a stronger foundation for every credit decision that follows. Moving from PDF to credit-ready isn’t about shortcuts. It’s about building workflows that support accuracy, scale, and confident lending decisions.

If your credit team is spending too much time wrestling with PDFs instead of evaluating deals, it may be time to rethink how business financials enter your workflow. Learn how FlashSpread helps lenders turn documents into credit-ready data with greater speed and confidence.