Mortgage lenders spend significant time and money getting borrowers to start an application. Marketing campaigns, referral relationships, digital ads, and outreach all funnel prospects toward that first step. But for many lenders, the real problem isn’t attracting applicants; it’s what happens after they click “Start Application.”

Application abandonment has become one of the most costly and least visible issues in mortgage lending. When borrowers stall or exit mid-process, lenders lose more than a potential loan. They lose marketing investment, loan officer time, operational efficiency, and future revenue opportunities. And because abandonment happens before underwriting or closing, its financial impact often goes unnoticed.

As margins tighten and origination costs remain elevated, lenders can no longer afford to treat abandonment as an inevitable byproduct of digital lending. It’s a solvable problem—and one that directly impacts revenue, efficiency, and borrower trust. Understanding the real cost of application abandonment is the first step toward fixing it.

Key Insights at a Glance

- Application abandonment creates hidden revenue loss long before loans reach underwriting.

- Drop-offs waste marketing spend, loan officer time, and operational capacity.

- Borrowers abandon applications due to complexity, uncertainty, and slow follow-up.

- Small improvements in completion rates can produce outsized revenue gains.

- BrightLite is designed to help lenders stop abandonment and convert more applications without added operational burden.

Why Application Abandonment Hurts More Than It Appears

On the surface, an abandoned application looks like a missed opportunity. In reality, it’s much more expensive.

Each incomplete application represents:

- Paid lead acquisition that never turns into revenue

- Partial data entry and processing that goes unused

- Loan officer attention diverted from qualified borrowers

- Pipeline metrics that look healthy but don’t convert

Unlike declined loans, abandoned applications often aren’t tracked with the same rigor. They don’t show up in fallout reports or underwriting statistics. Yet they quietly erode profitability by inflating cost per funded loan and stretching teams thin.

Over time, this compounds. Lenders are forced to spend more to originate the same volume, increasing pressure on both budgets and staff.

The Borrower Side of Abandonment

Borrowers rarely abandon applications because they lose interest in homeownership. More often, they leave because the process becomes overwhelming or unclear.

Common abandonment triggers include:

- Lengthy forms with repetitive questions

- Confusing documentation requirements

- No visibility into progress or next steps

- Delayed responses after submission

- Inability to complete tasks easily on mobile

When borrowers don’t know what’s expected, or feel unsure if they’re “doing it right”, they pause. And in today’s market, pausing often means leaving entirely.

The Operational Cost Lenders Don’t See

Abandonment doesn’t just affect borrowers. It directly impacts internal teams.

Loan officers spend time following up on partial applications that never convert. Processors field questions from applicants who don’t understand what’s required. Marketing teams keep pouring budget into top-of-funnel activity to compensate for low conversion downstream.

The result is a cycle where:

- More leads are required to hit the same production targets

- Staff workload increases without corresponding revenue

- Cost per loan continues to rise

This is how abandonment quietly becomes an operational tax across the organization, one that grows heavier as volume increases.

Why Fixing Abandonment Doesn’t Mean Adding Staff

The instinctive response to low conversion is often to add manual touchpoints: more follow-ups, more reviews, more people. But that approach increases costs without addressing the root cause.

The real issue is friction at the front of the funnel.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Reducing abandonment is less about working harder and more about designing a process that helps borrowers finish what they start. When applications are intuitive, guided, and responsive, fewer people drop off, and teams don’t need to chase them.

What Actually Reduces Application Abandonment

Lenders who successfully reduce abandonment focus on a few high-impact areas:

- Clarity: Borrowers need to understand what’s required, why it matters, and what comes next.

- Guidance: Step-by-step workflows and in-context prompts keep applicants moving forward.

- Speed: Automated reminders and real-time status updates maintain momentum.

- Accessibility: Mobile-friendly tools allow borrowers to complete tasks on their own schedule.

These changes don’t require rethinking your entire operation. They require fixing the moments where borrowers hesitate most.

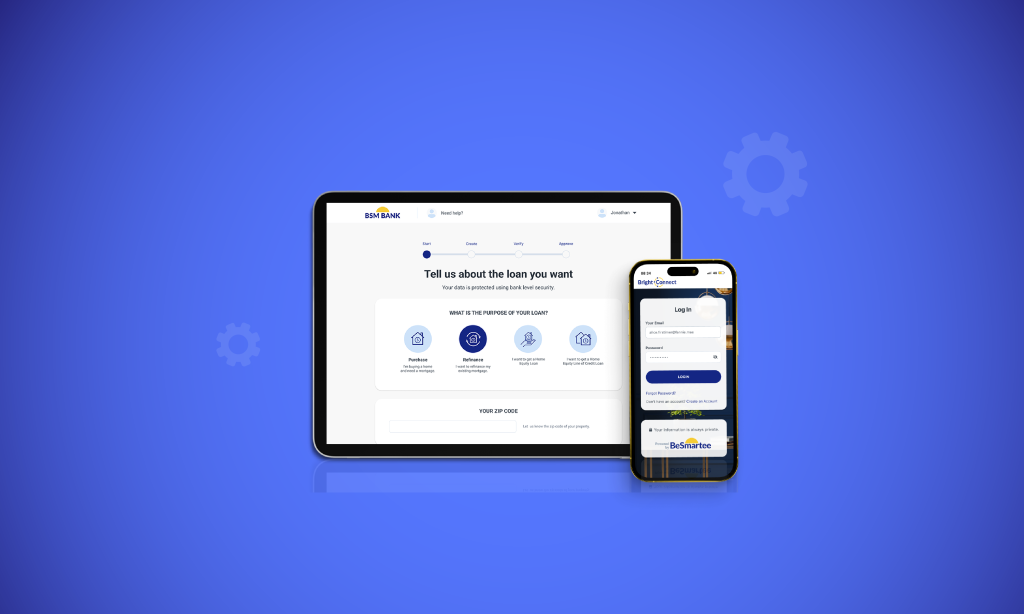

Where BrightLite Fits In

This is where BrightLite plays a role, not as a full POS replacement, but as a conversion-focused revenue engine built to stop application abandonment.

BrightLite is designed to strengthen the front end of the mortgage funnel by helping borrowers complete applications and submit required information with confidence. Its purpose-built approach focuses on improving submission rates without introducing additional operational burden.

Key BrightLite capabilities include:

- Pre-configured, best-practice workflows that guide borrowers step by step

- Intelligent automation that reduces manual follow-up for staff

- Integrated application and credit within Encompass®

- A mobile companion app for document uploads and status visibility

- Configurable branding and lender templates for a consistent borrower experience

With reported 80–85% application submission rates, BrightLite demonstrates how addressing abandonment directly can unlock more revenue from existing lead flow, without increasing headcount or technology overhead.

For lenders, that means fewer stalled starts, cleaner pipelines, and faster time to value from the leads they already have.

Quick Q&A

Q: Is application abandonment really a technology problem?

A. Often, yes. While borrower intent matters, unclear workflows, poor guidance, and slow feedback are major contributors that technology can address.

Q: Can reducing abandonment really move revenue numbers?

A. Absolutely. Even small lifts in completion rates can translate into meaningful increases in funded loans, especially for high-volume lenders.

Q: Do lenders need a full POS replacement to fix abandonment?

A. Not necessarily. Many lenders see strong results by improving the intake and submission experience first.

Roundup

Application abandonment is one of the most expensive problems in mortgage lending, and one of the least visible. It quietly inflates acquisition costs, drains operational capacity, and limits growth without ever appearing in traditional reports.

By focusing on improving completion at the top of the funnel, lenders can unlock more revenue from the same leads, the same teams, and the same marketing spend, without adding operational strain.

Ready to stop losing revenue before loans even reach underwriting? Discover how BrightLite helps lenders reduce application abandonment and convert more applications—efficiently, predictably, and without added overhead.