In commercial lending, credit teams rarely receive a perfectly packaged file. A borrower may submit business tax returns, income statements, balance sheets, rent rolls, debt schedules, bank statements, ownership documents, and supporting schedules, all in different formats and from different preparers.

Yet many lending workflows are still designed around a narrow set of standard documents. When a file includes something outside the expected path, the process slows down. Analysts may need to review the document manually, rekey information into spreadsheets, ask for clarification, or rely on workarounds that are not always repeatable across the team.

That is why document coverage matters. It is not just a technical product capability. It directly affects how quickly lenders can understand a borrower, how consistently teams can review financials, and how confidently credit decisions move forward.

This blog explores why broader document coverage is becoming more important in commercial credit review, where limited coverage creates friction, and how better document support can help lenders reduce manual work without sacrificing control.

Key Insights at a Glance

- Commercial credit files often include more than standard business tax returns

- Limited document coverage forces analysts into manual workarounds

- Broader document support improves speed, consistency, and review confidence

- Less common documents can still carry important credit context

- Better coverage helps teams scale review across more borrower types

- Strong document workflows reduce rework before underwriting and approval

Table of Contents

- Commercial Credit Files Are Getting More Complex

- The Problem With Narrow Document Support

- Why Less Common Documents Still Matter

- Document Coverage Impacts Decision Speed

- Document Coverage Also Impacts Consistency

- The Role of Validation in Document Coverage

- Q&A: Document Coverage in Credit Review

- Building a More Complete Credit Review Workflow

- How FlashSpread Supports Broader Document Coverage

- Roundup

Commercial Credit Files Are Getting More Complex

Commercial lending is not one-size-fits-all. A small business borrower, a real estate entity, a nonprofit, an association, or a multi-entity ownership group may each submit different financial documentation. Even when the credit question is similar, the supporting documents can vary significantly.

A standard C-corp borrower may provide a Form 1120. A pass-through entity may submit an 1120-S or 1065. A real estate-heavy borrower may include rental schedules, operating statements, or supporting property income documentation. Some entities may submit company-prepared income statements and balance sheets, while others rely heavily on tax returns.

This document variety is normal in commercial lending, but it can create operational strain when systems and processes are only built around the most common forms. The more document types a team has to handle manually, the more likely the review process becomes inconsistent.

Document coverage becomes especially important when credit teams are trying to support growth. More loan volume often means more borrower variety, more document variation, and more exceptions to standard workflow assumptions.

The Problem With Narrow Document Support

When a system only handles a limited set of documents well, the rest of the work does not disappear. It shifts back to the analyst.

That creates several common problems:

- Analysts spend time manually extracting information

- Different team members handle uncommon documents differently

- Review standards become harder to maintain

- Data may not flow cleanly into reports or exports

- Less common borrower types take longer to process

This can make lenders more efficient on simple files while still struggling with complex ones. The result is an uneven credit review experience. Straightforward borrowers move quickly, while anything outside the standard path creates delays and rework.

For lenders trying to serve a broader range of businesses, that inconsistency matters. It affects borrower experience, credit desk capacity, and the team’s ability to compete for more complex opportunities.

Why Less Common Documents Still Matter

It is easy to focus on the documents that appear most often. But less common forms and supporting documents can still carry important credit context.

For example, certain business tax returns may reveal entity-specific income, deductions, payments, or ownership structures that affect how the borrower should be evaluated. Supporting documents may explain property income, debt obligations, liquidity, operating performance, or compliance details.

When these documents fall outside automated review, analysts must bridge the gap manually. This may involve checking totals, validating calculated lines, interpreting supporting schedules, or deciding how to incorporate the information into the broader spread.

These steps are not optional. They shape the quality of the credit decision.

The risk is that uncommon documents become operational blind spots. If they are reviewed inconsistently or excluded from structured workflows, credit teams may lose valuable context or spend too much time reconstructing it manually.

Document Coverage Impacts Decision Speed

Credit review speed depends on more than how quickly the main return is processed. It depends on how smoothly the full financial package moves through the workflow.

When document coverage is limited, delays often appear in small but repeated ways:

- A document must be manually reviewed outside the system

- A calculated value does not tie out and requires investigation

- A supporting schedule must be rekeyed into a spreadsheet

- A less common form requires senior analyst review

- Data from one document cannot easily connect to another

Each delay may seem manageable on its own. Across a full pipeline, however, these small slowdowns compound.

Decision speed depends on reducing the number of places where analysts have to stop, switch tools, or rebuild information manually. Broader document support helps keep more of the review process inside a consistent workflow.

Document Coverage Also Impacts Consistency

Speed is important, but consistency may matter even more.

When uncommon or unsupported documents are handled manually, different analysts may interpret the same type of document differently. One reviewer may map a line item one way. Another may treat it differently. A third may exclude it from the spread entirely if the workflow does not provide a clear place for it.

Over time, this creates variation in how borrowers are evaluated. Similar files may produce different outputs depending on who handled the document and how much time they had to review it.

Broader document coverage helps reduce that variation by giving teams a more consistent way to extract, validate, and structure information. It does not remove analyst judgment. It gives analysts a cleaner and more repeatable starting point.

That consistency becomes increasingly important as teams grow, train new analysts, or expand into new borrower segments.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

The Role of Validation in Document Coverage

Document coverage is not just about recognizing more documents. It is also about validating the information inside them.

For commercial credit review, validation helps answer basic but critical questions:

- Do totals calculate correctly?

- Are related fields in balance?

- Are required values present?

- Has an override or correction been documented?

- Can reviewers see what changed and why?

This matters because credit teams need both flexibility and control. Not every exception should block a review, but exceptions should be visible, justified, and traceable.

For example, validation policies can help flag out-of-balance calculated lines, allow authorized corrections or overrides, and maintain audit history around field changes or hidden errors. In FlashSpread’s internal validation specifications for a prioritized business tax form, validation rules include calculated-line checks, severity classifications, override behavior, and audit logging requirements for field changes and hidden errors.

This type of structure helps lenders maintain confidence when reviewing more document types. It also helps ensure that speed does not come at the expense of review quality.

Q&A: Document Coverage in Credit Review

Q: Does broader document coverage mean every document is fully automated?

A. Not necessarily. Coverage can include classification, extraction, validation, routing, or support for review workflows. The goal is to reduce manual friction where possible while keeping analysts in control.

Q: Why not just focus on the most common forms first?

A. Common forms should be prioritized, but lenders still encounter files that include less common returns and supporting documents. If those documents fall outside the workflow, they can slow otherwise strong deals.

Q: Does document coverage matter for smaller lenders?

A. Yes. Smaller teams often feel the impact most because they have fewer analysts available to handle manual exceptions. Better coverage helps lean teams manage variety without adding unnecessary headcount.

Building a More Complete Credit Review Workflow

A stronger document workflow starts with a simple idea: the credit file should not fall apart when it includes something beyond the standard package.

To get there, lenders should evaluate their current process across four areas.

First, identify which documents appear most often and which ones create the most manual work. The most common documents are not always the biggest source of friction.

Second, review where analysts leave the main workflow. If a team has to use spreadsheets, email threads, or separate manual reviews for specific document types, that is a sign of incomplete coverage.

Third, evaluate how exceptions are handled. Corrections and overrides are normal, but they should be visible and documented.

Finally, consider how information flows downstream. If document data does not move cleanly into reports, analysis, or exports, the team may still be relying too heavily on manual bridge work.

The objective is not to automate every possible document immediately. It is to keep more of the credit review process structured, traceable, and repeatable.

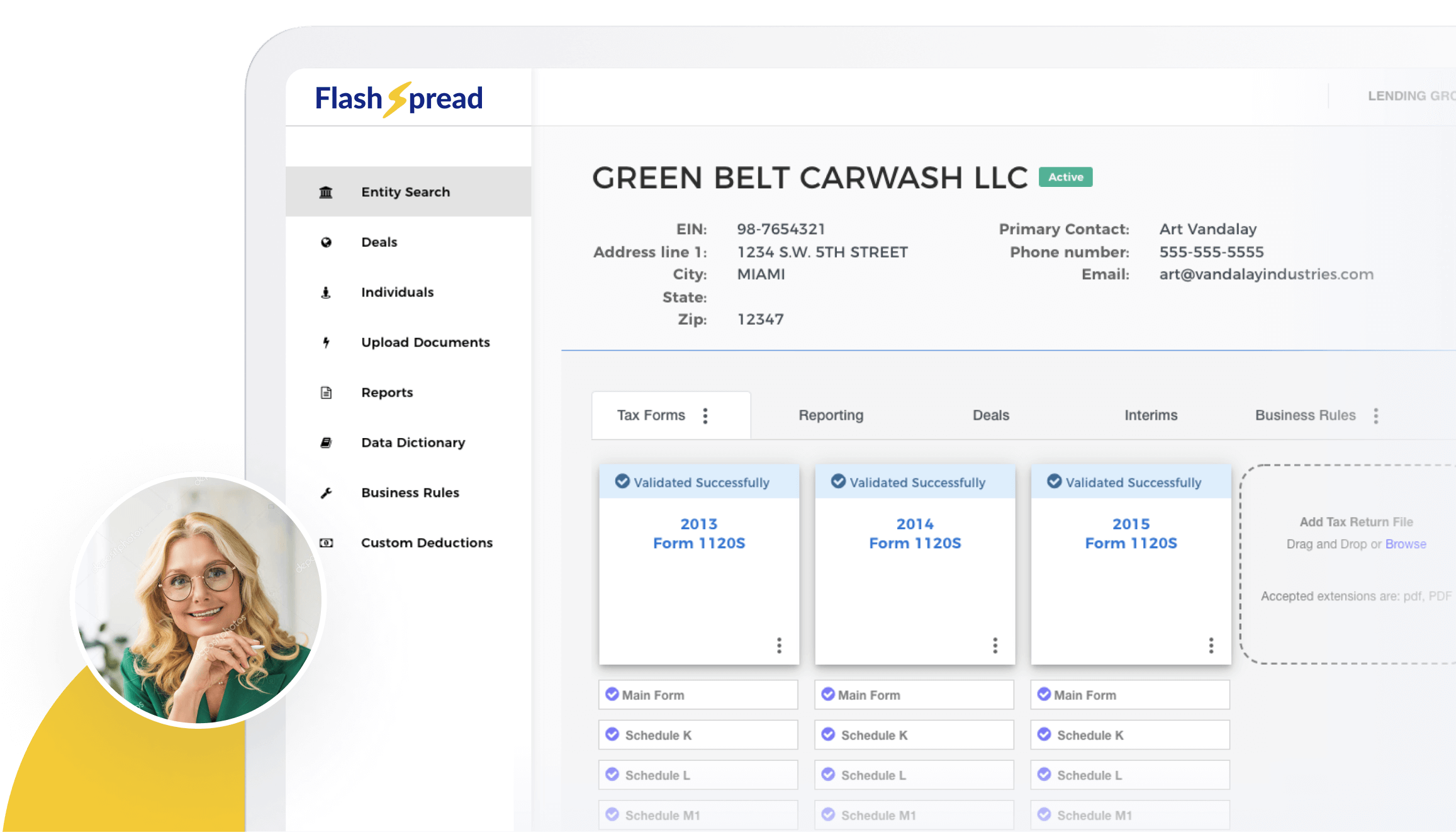

How FlashSpread Supports Broader Document Coverage

FlashSpread is built around the reality that commercial credit files include more than one type of document.

Product materials show support and prioritization across a broad range of commercial lending documents, including common business tax returns, business financials such as income statements and balance sheets, and additional documents tied to debt, liquidity, verification, valuation, collateral, and compliance workflows.

The internal document priority list also identifies several structured business tax returns and business financials as part of the financial engine, including income statements and balance sheets marked complete, and Form 1120-H listed as prioritized.

Using document upload, OCR, and AI, FlashSpread helps digitize and extract financials without relying on manual data entry. It also supports validation, error detection, reporting, analytics, integrations, and exports that help lenders simplify credit review and downstream workflows.

For lenders, this means broader document coverage can support:

- Faster review across more borrower scenarios

- More consistent financial data preparation

- Reduced manual rekeying and exception handling

- Cleaner reporting and exports

- Better confidence when reviewing complex credit files

The goal is not just to process documents faster. It is to help lenders handle document variety without losing structure, accuracy, or control.

Roundup

Commercial credit review depends on more than the most common tax returns. Real borrower files include a wider mix of documents, from business returns and financial statements to schedules, verification documents, and supporting materials.

When document coverage is limited, credit teams are forced to fill the gaps manually. That slows decisions, creates inconsistency, and makes complex files harder to review at scale.

Broader document coverage helps lenders keep more of the credit review process structured. It improves speed, supports consistency, and gives analysts more confidence when working across borrower types and document formats.

If document gaps are slowing your credit reviews, it may be time for broader coverage. See how FlashSpread helps turn more borrower documents into decision-ready data.