For years, the Loan Origination System (LOS) has been viewed as the natural next step for growing lending teams. As workflows became more complex, lenders adopted larger systems to centralize operations, manage documentation, and standardize approvals.

But many commercial lenders today are finding themselves in a different position. They have outgrown spreadsheets and manual workflows, yet a LOS can still feel too expensive, too rigid, or too operationally heavy for what they actually need. In many cases, the biggest bottlenecks are not across the entire lending lifecycle. They are concentrated inside the credit process itself.

This is driving the rise of a new operational model: the AI-enabled core credit workflow. More than a spreading tool but lighter than a traditional LOS, this approach focuses on streamlining document intake, financial analysis, and underwriting workflows first. This blog explores why more lenders are adopting core credit workflows and how tools like FlashSpread are becoming the operational center of modern credit teams.

Key Insights at a Glance

- Many lenders have outgrown spreadsheets but are not ready for a LOS

- Traditional LOS platforms can introduce cost and operational complexity

- Credit workflows are becoming the operational center of lending

- AI-enabled workflows improve speed, structure, and scalability

- Core credit workflows bridge the gap between manual processes and enterprise systems

- FlashSpread supports lenders as a scalable core credit workflow engine

- The Gap Between Spreadsheets and Enterprise Systems

- Why Credit Has Become the Starting Point

- What Defines a Core Credit Workflow

- Where Traditional Workflows Lose Efficiency

- Q&A: Understanding the Credit-First Model

- How FlashSpread Fits Into the Shift Toward Core Credit Workflows

- A Different Way to Modernize Lending Operations

- Roundup

The Gap Between Spreadsheets and Enterprise Systems

Many commercial lenders operate in an uncomfortable middle ground.

Their workflows have become too complex for spreadsheets and email-driven processes, but implementing a LOS may still feel excessive for their operational needs.

This often creates fragmented workflows:

- Borrower documents arrive through email

- Financial spreading happens in spreadsheets

- Credit memos live in separate files

- Deal tracking occurs across disconnected tools

- Policy interpretation depends on senior analysts

Over time, these disconnected processes create friction:

- Manual data entry slows decisions

- Rework loops increase analyst workload

- Visibility across deals becomes limited

- Scaling requires additional headcount

The natural reaction is often to evaluate a LOS. However, many institutions discover that enterprise systems introduce their own challenges:

- Long implementation cycles

- Significant upfront investment

- Rigid workflow structures

- Ongoing maintenance overhead

For smaller and growing teams, the question becomes less about replacing spreadsheets with a massive system and more about introducing the right amount of operational structure.

Why Credit Has Become the Starting Point

In commercial lending, the most operationally intensive work happens inside underwriting.

This is where teams:

- Review borrower financials

- Validate data accuracy

- Interpret policy

- Evaluate risk

- Prepare decision-ready analysis

In other words, this is where decision velocity is created or lost.

As lenders modernize, many are recognizing that improving the credit workflow delivers disproportionate operational impact. Instead of attempting to centralize everything at once, they focus first on the stages that consume the most time and create the most bottlenecks.

This “credit-first” approach creates several advantages:

Faster Operational Improvement

Teams can modernize the most painful parts of the workflow immediately instead of waiting for a full platform rollout.

Lower Complexity

Instead of redesigning the entire lending operation, institutions improve targeted workflow stages incrementally.

Better Scalability

Structured workflows allow teams to process more deals without linear headcount growth.

Greater Flexibility

Credit workflows can evolve alongside the institution rather than forcing teams into rigid processes prematurely.

The result is a more practical modernization path.

What Defines a Core Credit Workflow

Core credit workflow does not refer to a simplified LOS clone. It represents a different philosophy.

Traditional LOS platforms are designed to manage the entire lending lifecycle within a centralized system.

The emerging core credit workflow model focuses instead on becoming the operational core of the credit process itself.

That means providing structure around:

- Document intake

- Financial spreading

- Data validation

- Credit analysis

- Workflow visibility

- Underwriting support

Importantly, it is more than a standalone spreading tool.

A spreading tool solves one task. A core credit workflow engine supports how deals move from intake to decision.

This distinction matters because many lenders are not simply trying to automate data extraction. They are trying to create repeatable, scalable underwriting operations without introducing unnecessary system overhead.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

Where Traditional Workflows Lose Efficiency

To understand why this shift is happening, it helps to examine where time is lost today.

Manual Financial Spreading

Income statements, balance sheets, and tax returns arrive in inconsistent formats. Analysts spend hours rekeying, validating, and restructuring data before meaningful analysis can begin.

Disconnected Workflow Stages

Documents, analysis, communication, and approvals often live across separate systems or spreadsheets. This creates friction and reduces visibility.

Rework Loops

When inconsistencies surface during underwriting, files must be corrected and recalculated. The same data may be touched multiple times before a decision is finalized.

Analyst Dependency

Many workflows rely heavily on institutional memory and senior staff guidance, particularly during policy interpretation or exception handling.

These inefficiencies compound as volume increases. Eventually, the process itself becomes the bottleneck.

Q&A: Understanding the Credit-First Model

Q: Does this replace a traditional LOS entirely?

A. Not necessarily. For some lenders, a LOS remains appropriate. For others, an AI-enabled core credit workflow provides the structure they need without enterprise-level complexity.

Q: Is this only for smaller lenders?

A. No. Many institutions use modular workflows strategically, even alongside larger systems.

Q: How is this different from a spreading tool?

A. A spreading tool automates extraction. A core credit workflow supports intake, structuring, analysis, and operational visibility across underwriting.

How FlashSpread Fits Into the Shift Toward Core Credit Workflows

FlashSpread is designed around this credit-first philosophy.

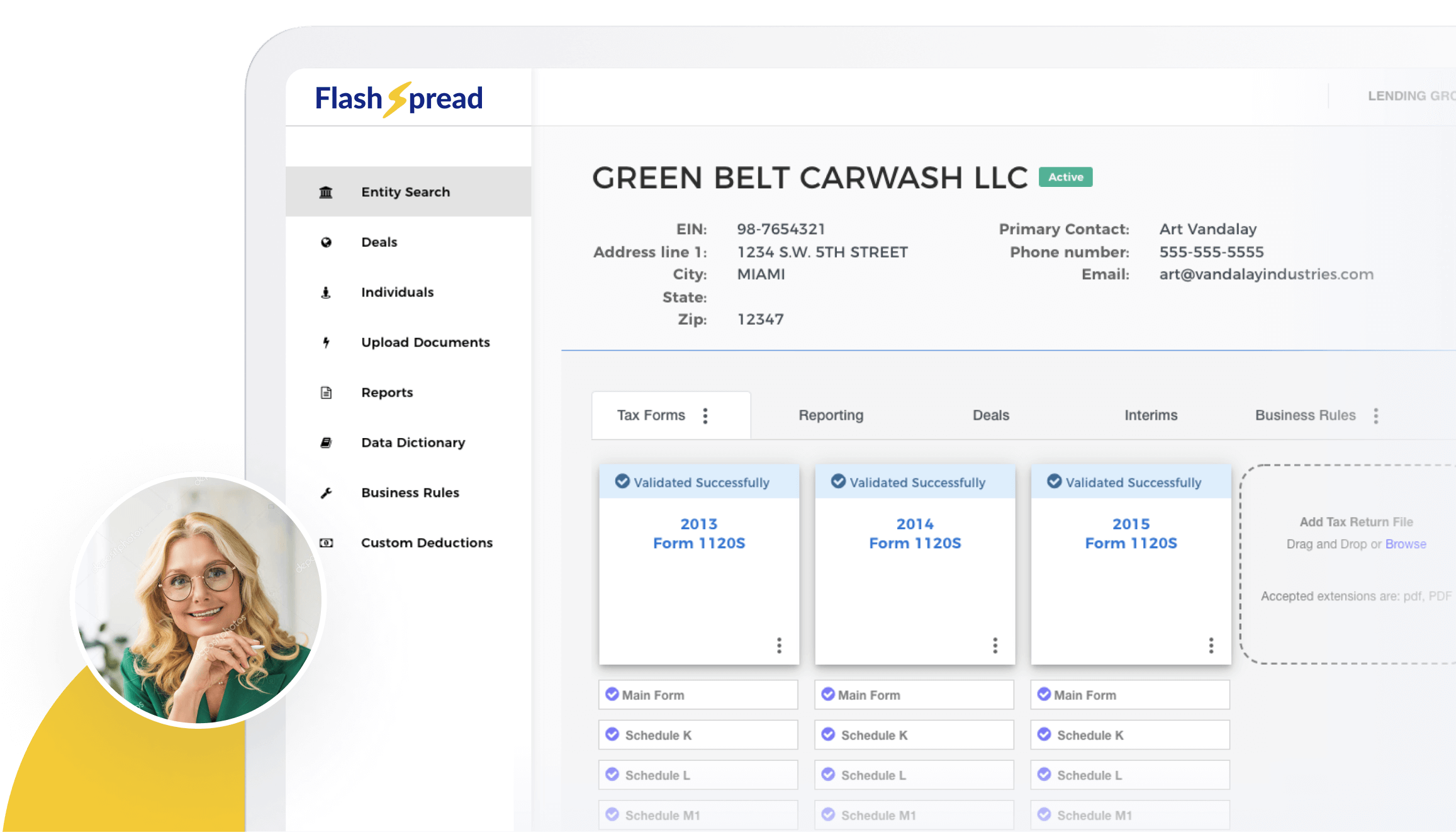

Rather than functioning solely as a financial spreading tool, FlashSpread acts as an AI-enabled core credit workflow that supports teams from document intake through underwriting preparation.

Using OCR and machine learning, FlashSpread extracts and organizes financial data from tax returns, income statements, and balance sheets. The system standardizes this data into a structured format that supports faster review and cleaner downstream analysis.

But the workflow extends beyond extraction.

FlashSpread also helps centralize the operational flow around credit by supporting:

- Document intake and organization

- Structured financial data preparation

- Validation and categorization workflows

- Consistent analysis across deals

- AI-powered underwriting guidance and policy support through AskFlash

- Faster resolution of credit policy questions with source-cited answers and escalation support

- Improved visibility into underwriting operations

As more business financials are processed, the system learns categorization behavior and common patterns, helping streamline future reviews and reduce repetitive manual work.

For lean lending teams, this creates a practical operational core. Teams gain the structure needed to scale without immediately taking on the cost and complexity of a LOS implementation.

This is why core credit workflows are gaining traction. They offer a middle path between manual workflows and heavyweight systems.

A Different Way to Modernize Lending Operations

Historically, lending modernization was treated as a large-scale system decision.

Today, many lenders are approaching it differently. Instead of beginning with enterprise infrastructure, they begin with operational friction.

- Where are analysts losing time?

- Where do rework loops occur?

- Where does decision velocity slow down?

By solving these workflow bottlenecks first, institutions can modernize incrementally while still improving scalability, consistency, and speed.

This is less about replacing systems and more about creating operational leverage.

Roundup

Not every lender needs a LOS to build an effective lending operation. For many growing institutions, the immediate need is not enterprise infrastructure. It is a structured, scalable credit workflow that improves decision velocity without adding operational complexity.

This is why more lenders are starting with credit first. The rise of core credit workflows reflects a broader shift toward AI-enabled operational models that centralize intake, financial spreading, analysis, and underwriting support in a more flexible way.

If your team has outgrown spreadsheets but isn’t ready for the cost and complexity of a LOS, it may be time to rethink what modern lending infrastructure actually looks like.