In commercial lending, experience shapes outcomes. Over time, senior credit officers develop a refined understanding of risk that goes beyond documented thresholds and ratio guidance. They understand how precedent influences interpretation, when qualitative strengths may offset quantitative weaknesses, and where institutional risk appetite truly sits in practice.

That accumulated judgment becomes the backbone of consistent underwriting.

The challenge is that, in many institutions, this expertise lives primarily with people rather than in systems. It exists in conversations, email threads, meeting notes, and the accumulated experience of a small group of senior analysts. While this model may function effectively in stable environments, it creates a structural vulnerability during periods of growth, turnover, or organizational change.

The issue is not competence. It is continuity. When institutional credit philosophy is not embedded into operational infrastructure, consistency depends on availability rather than design.

Key Insights at a Glance

- Institutional credit judgment often resides in individuals rather than structured systems

- Senior analyst dependency creates operational and continuity risk

- Searching policy is not the same as interpreting policy in context

- Growth and turnover amplify interpretive variability

- Underwriting intelligence embeds institutional philosophy into daily workflows

- AI strengthens continuity without replacing human decision authority

The Structural Risk of Senior Analyst Dependency

Most commercial credit teams rely heavily on a relatively small group of experienced professionals. These individuals are frequently consulted to:

- Interpret complex policy scenarios

- Resolve gray-area underwriting questions

- Guide exception approvals

- Provide historical precedent

- Clarify how competing risk factors should be weighed

Their expertise ensures quality and alignment. However, it also creates concentration risk. When interpretive authority is concentrated in a few individuals, several operational pressures emerge:

- Escalation bottlenecks that slow decision cycles

- Increased cost per decision due to manual Q&A filtering

- Variability depending on which senior officer responds

- Knowledge vulnerability during retirement or turnover

Over time, informal reliance on specific individuals becomes embedded into workflow habits. Escalation becomes default rather than exception. Consistency depends on memory rather than system design.

This dependency rarely appears as a formal risk on reports. Yet it directly affects scalability and governance durability.

Policy Search vs. Policy Interpretation

Many institutions attempt to reduce dependency risk by centralizing policy documentation. SharePoint repositories are organized. PDFs are indexed. Search functions improve.

These efforts are valuable but incomplete. There is a fundamental difference between policy search and policy interpretation.

Policy search answers a logistical question: Where is the relevant section located?

Policy interpretation answers a more complex one: How should this guidance apply to the specific borrower, structure, or industry scenario in front of me?

Commercial credit policies define limits, thresholds, procedures, and documentation standards. They rarely capture nuance such as:

- How qualitative compensating factors have historically influenced decisions

- When exceptions were tolerated and why

- How sector volatility impacted prior interpretations

- How competing risk signals were balanced

Keyword search does not resolve contextual ambiguity. That is why even well-trained analysts escalate questions despite having access to documentation. The friction lies not in locating policy but in applying it consistently with institutional philosophy.

Without structural reinforcement, interpretation becomes uneven.

Why Informal Knowledge Transfer Doesn’t Scale

Traditionally, underwriting judgment is transferred through mentorship. Junior analysts observe senior colleagues, internalize reasoning patterns, and gradually develop similar instincts.

This apprenticeship model works in stable environments. It becomes fragile during expansion or transition.

During growth phases:

- New analysts onboard rapidly

- Policy-related questions increase in volume

- Senior staff field repetitive clarifications

- Decision timelines lengthen

During transition phases:

- Retirements remove historical context

- Leadership changes subtly shift interpretation

- Institutional memory fragments

The result is not deliberate policy deviation. It is gradual interpretive drift.

When institutional judgment is not embedded into infrastructure, each personnel change introduces variability. Over time, risk posture may evolve unintentionally.

The Governance Implications

The consequences of expertise living outside systems extend beyond operational friction.

1. Consistency Risk

Similar borrower scenarios may produce different interpretations depending on who responds to the question.

Subscribe to BeSmartee 's Digital Mortgage Blog to receive:

- Mortgage Industry Insights

- Security & Compliance Updates

- Q&A's Featuring Mortgage & Technology Experts

2. Audit Exposure

If guidance is delivered through informal channels such as email or conversation, traceability becomes limited.

3. Cost Per Decision

Manual filtering of repetitive policy questions increases overhead and consumes SME capacity.

4. Strategic Drift

Incremental interpretive shifts may slowly alter institutional risk appetite without explicit policy revision.

In aggregate, these factors weaken alignment between written standards and applied behavior.

Q&A: Addressing Common Questions

Is variability always a problem?

A. Discretion is necessary in commercial lending. The objective is not rigid uniformity but consistent alignment with institutional philosophy.

Can documentation alone solve this issue?

A. Documentation provides reference. It does not guarantee real-time accessibility or consistent interpretation.

Is AI replacing credit officers?

A. No. The objective is continuity and accessibility, not delegation of decision authority.

Embedding Institutional Judgment Through Underwriting Intelligence

To institutionalize credit philosophy, institutions need more than searchable documentation. They require structured underwriting intelligence that operates at the moment of decision.

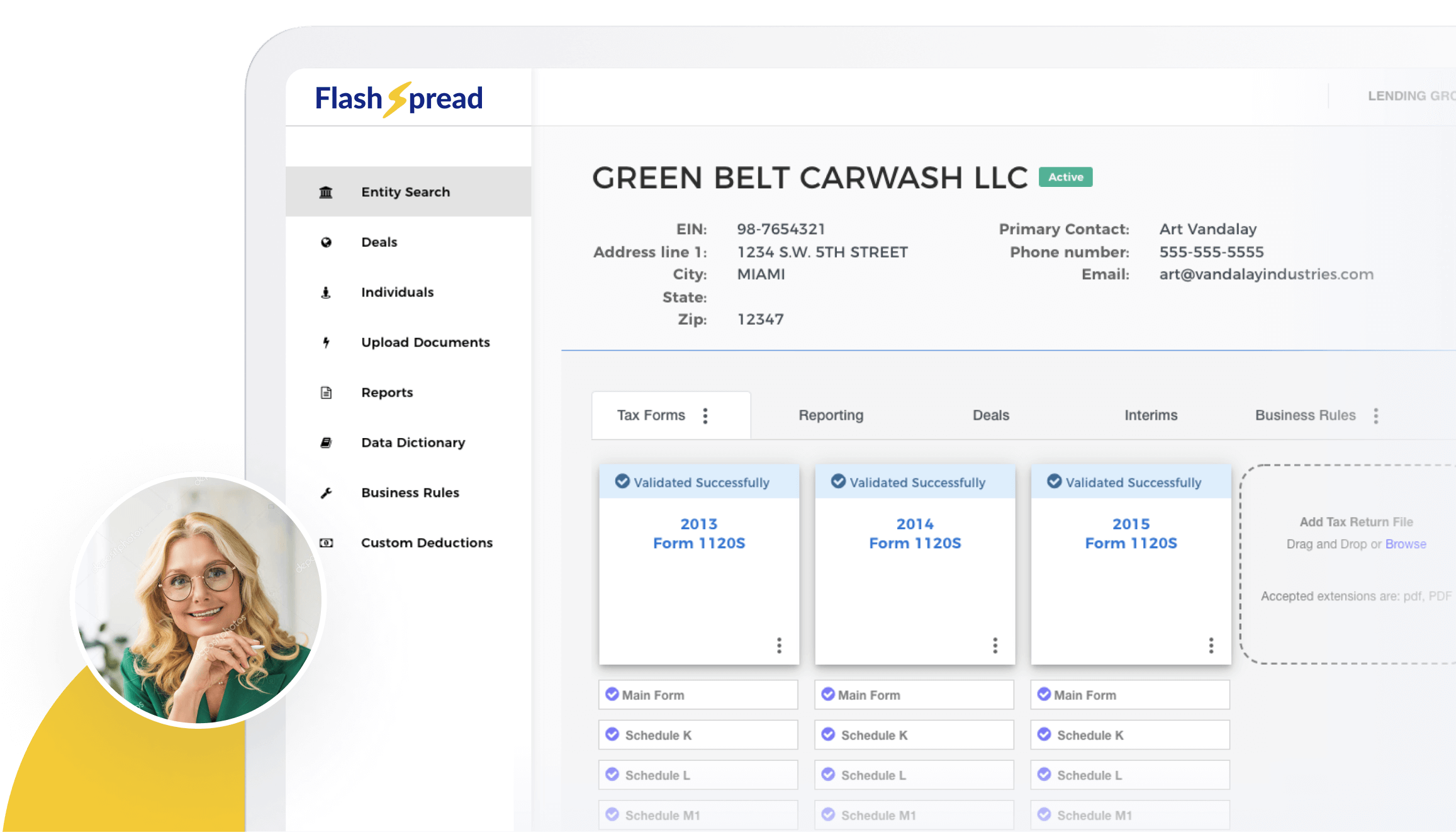

FlashSpread Credit Desk Underwriting Intelligence provides that structural layer. It functions as an AI-powered assistant trained on an institution’s credit policies and internal knowledge sources. Analysts can submit policy-related questions through embedded web chat, SMS, or email and receive fast, source-cited responses drawn directly from approved documentation.

Key capabilities include:

- Credit Q&A Assistant: Context-aware answers grounded in institutional policy

- Multi-Policy Decisioning: Evaluation of a single question across multiple policy documents

- Human-in-the-Loop Escalation: Automatic routing of uncertain queries to the appropriate SME, with responses captured for future reference

- Bulk Scenario Testing: Validation of large question sets for audit or quality review

- Role-Based Tuning: Adjusted response depth based on user profile

By automating approximately 90% of repetitive policy Q&A, the system reduces escalation bottlenecks while preserving human oversight for nuanced cases. When senior analysts provide clarification, that expertise becomes part of the institutional knowledge base rather than remaining isolated in correspondence.

Implementation is designed for minimal disruption. Institutions can connect existing policy repositories such as SharePoint or Google Drive, normalize guideline structures for reliability, and deploy delivery channels in a matter of weeks. The outcome is not automation for its own sake. It is structured continuity.

AI as Continuity Infrastructure, Not Replacement

In underwriting environments, accountability and governance are paramount. Any technological enhancement must reinforce rather than dilute professional oversight.

Underwriting intelligence supports credit teams by:

- Ensuring consistent, source-cited policy access

- Structuring escalation pathways

- Preserving interpretive insight

- Strengthening audit traceability

Senior credit officers remain central to complex judgment. AI does not replace experience. It amplifies its reach and durability. Institutional philosophy becomes embedded infrastructure rather than informal memory.

Preserving Institutional Risk Philosophy at Scale

Every commercial lender has a distinct risk identity shaped by history, leadership, and market positioning. This philosophy influences how trade-offs are evaluated, how qualitative strength is weighed, and how exceptions are handled. If that philosophy resides only in individuals, it is inherently fragile. If embedded into underwriting intelligence, it becomes resilient.

Institutionalizing credit judgment does not constrain flexibility. It ensures that flexibility operates within consistent guardrails. It protects continuity during leadership transitions. It supports scalability during growth. It strengthens governance without slowing decision-making. In an environment defined by workforce evolution and increasing complexity, preserving institutional knowledge is not optional. It is strategic infrastructure.

Roundup

Commercial lending depends on expertise. But when expertise lives primarily in individuals, continuity becomes vulnerable.

Senior analyst dependency creates bottlenecks and concentration risk. Policy search does not equal policy interpretation. Informal knowledge transfer does not scale reliably.

Institutionalizing credit judgment requires embedding risk philosophy into structured, accessible systems. Underwriting intelligence provides that foundation, ensuring policy interpretation is consistent, traceable, and durable across personnel changes.

If your credit function relies heavily on a small group of experienced decision-makers, it may be time to evaluate how that knowledge is being preserved. Explore how FlashSpread supports continuity while keeping human judgment at the center.